Unveiling Rogers (ROG)'s Value: Is It Really Priced Right? A Comprehensive Guide

Rogers Corp (NYSE:ROG) has recently made headlines with its daily loss of 3.51% and a three-month loss of 17.11%. Despite these figures, the company's Earnings Per Share (EPS) stands at a respectable 5.13. This begs the question: is Rogers (NYSE:ROG) significantly undervalued? In this article, we'll delve into a comprehensive valuation analysis of Rogers (NYSE:ROG) to uncover the answer.

Company Introduction

Rogers Corporation designs, develops, and manufactures engineered materials and components for sale to original equipment manufacturers and component suppliers. The company operates in three business segments: advanced connectivity solutions, elastomeric material solutions, and power electronics solutions. The firm generates revenue primarily in the United States, China, and Germany, but has a presence around the world.

As of September 26, 2023, Rogers (NYSE:ROG) has a stock price of $129.24 and a market cap of $2.40 billion. When compared to the GF Value of $7479.59, it appears that the stock may be significantly undervalued. Let's delve deeper into the financials to get a clearer picture.

Understanding the GF Value

The GF Value is a proprietary measure that estimates the current intrinsic value of a stock. It's calculated based on historical multiples, a GuruFocus adjustment factor based on past returns and growth, and future business performance estimates. The GF Value Line gives an overview of the fair value that the stock should be traded at. If the stock price is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. Conversely, if it is significantly below the GF Value Line, its future return will likely be higher.

Based on this method, Rogers (NYSE:ROG) appears to be significantly undervalued. Therefore, the long-term return of its stock is likely to be much higher than its business growth.

Link: These companies may deliever higher future returns at reduced risk.

Evaluating Financial Strength

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it's crucial to carefully review a company's financial strength before deciding whether to buy shares. Rogers has a cash-to-debt ratio of 1.08, which ranks worse than 54.61% of 2373 companies in the Hardware industry. However, GuruFocus ranks Rogers's financial strength as 8 out of 10, suggesting a strong balance sheet.

Profitability and Growth

Companies that have been consistently profitable over the long term offer less risk for investors. Rogers has been profitable 10 over the past 10 years. Over the past twelve months, the company had a revenue of $945.60 million and Earnings Per Share (EPS) of $5.13. Its operating margin is 6.41%, which ranks better than 61.99% of 2457 companies in the Hardware industry. Overall, the profitability of Rogers is ranked 7 out of 10, which indicates fair profitability.

One of the most important factors in the valuation of a company is growth. Companies that grow faster create more value for shareholders, especially if that growth is profitable. The average annual revenue growth of Rogers is2.2%, which ranks worse than 57.01% of 2333 companies in the Hardware industry. The 3-year average EBITDA growth is 19.8%, which ranks better than 65.43% of 1961 companies in the Hardware industry.

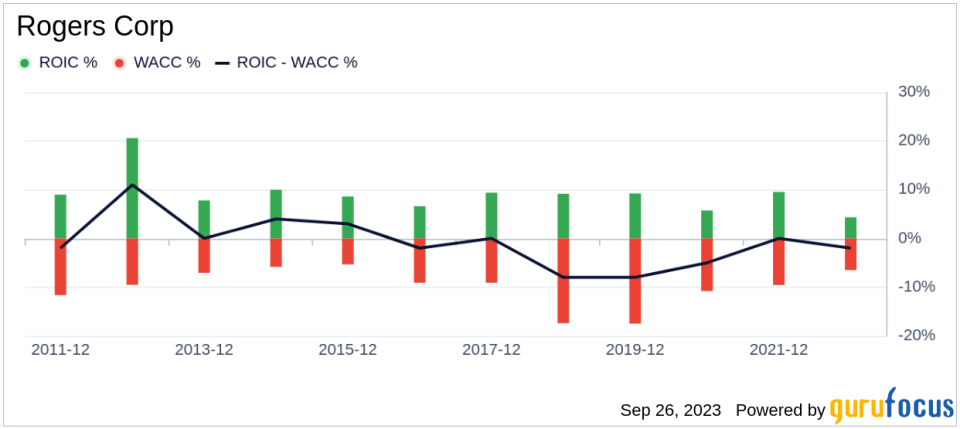

ROIC vs WACC

Comparing a company's return on invested capital (ROIC) to its weighted average cost of capital (WACC) can also evaluate its profitability. If the ROIC exceeds the WACC, the company is likely creating value for its shareholders. During the past 12 months, Rogers's ROIC is 3.79 while its WACC came in at 6.26.

Conclusion

In conclusion, the stock of Rogers (NYSE:ROG) appears to be significantly undervalued. The company's financial condition is strong and its profitability is fair. Its growth ranks better than 65.43% of 1961 companies in the Hardware industry. To learn more about Rogers stock, you can check out its 30-Year Financials here.

To find out the high quality companies that may deliever above average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.