Urban Outfitters (URBN) Appears a Promising Stock: Here's Why

Urban Outfitters, Inc. URBN seems a lucrative bet, thanks to its robust business strategies and solid fundamentals. URBN’s strategic growth initiative, which is the FP Movement, and store-growth endeavors are also impressive. Management has been strengthening its direct-to-consumer business, enhancing productivity across existing channels and optimizing inventory levels.

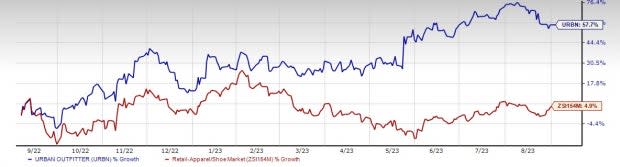

Such strengths have aided the shares of this Philadelphia, PA-based company to rally 57.7% in a year’s span, outperforming the industry’s 4.9% gain. Analysts look optimistic about this Zacks Rank #1 (Strong Buy) company. For fiscal 2024, the Zacks Consensus Estimate for URBN’s sales and earnings per share (EPS) is currently pegged at $5.11 billion and $3.18, respectively, suggesting 6.6% and 81.7% growth from the year-ago period’s corresponding figures.

For fiscal 2025, the consensus estimate for sales and EPS presently stands at $5.30 billion and $3.37, respectively, indicating an increase of 3.8% and 6% each from the previous fiscal year’s actuals. Let’s delve deeper.

Robust Strategies

Management has been making investments in the FP Movement with digital and creative brand prospects. It believes that the FP Movement will lure a wider base of customers to the Free People brand. Having a differentiated position in the fitness and wellness space, the FP Movement offers a major growth opportunity and is expected to boost Free People’s brand revenues.

Image Source: Zacks Investment Research

In addition, management remains optimistic about the prospects of Nuuly, which comprises the Nuuly Rent and Nuuly Thrift brands. During the fiscal second quarter, Nuuly, the subscription-based rental service for women’s clothes, contributed $55.8 million to net sales. This reflected an increase from $28.8 million recorded in the earlier fiscal year’s comparable period, backed by an 85% rise in active subscribers. Going forward, management remains optimistic about the prospects of Nuuly.

Being a multi-brand and multi-channel retailer, Urban Outfitters offers a flexible merchandising strategy. The company also has a significant domestic and international presence with rapidly expanding e-commerce activities. It also makes rational store-expansion endeavors. In fiscal 2024, management plans to open about 28 stores and close nearly 21 outlets.

What Else?

Buoyed by such tailwinds, the company reported sturdy results for second-quarter fiscal 2024, wherein the top and the bottom line beat the Zacks Consensus Estimate. Also, sales and earnings grew year over year. Brandwise, net sales were up 10.6% year over year at Anthropologie Group and 22% at Free People. Four of the company’s five brands saw record second-quarter revenues.

The Anthropologie, Free People and FP Movement brands recorded double-digit sales increases in stores and online. Customer demand for fashion at the Anthropologie, Free People and FP Movement brands was sturdy throughout the reported quarter. Customers responded positively to fashion innovation across women's apparel, accessories and shoe categories.

Management is pleased with the sturdy overall consumer demand at the start of the fiscal third quarter. This is likely to continue throughout the quarter. The third-quarter total company sales growth will be in the high-single digits, driven by mid-single-digit increase in Retail segment comp sales and high-double-digit growth in Nuuly. The company anticipates the gross margin for the quarter to improve more than 400 bps year over year, backed by increased initial product margins from reduced inbound freight costs and merchandise markdowns.

In the August-to-date period, total Retail segment comps were in line with the first-half results, and management expects total Retail segment comps in the third quarter to be very similar to both the preceding quarters. The company believes that the Free People Group's Retail segment performance will be nicely positive in the impending quarter. The strength in all the apparel and accessory categories has continued in August, which makes the company optimistic about Anthropologie delivering strong comps in the third quarter.

All in all, Urban Outfitters’ stock proves to be a solid investment bet now on the aforesaid strengths.

Eye These Solid Picks Too

We have highlighted three other better-ranked stocks, namely Abercrombie & Fitch ANF, Boot Barn BOOT and American Eagle Outfitters AEO.

Abercrombie & Fitch, a leading casual apparel retailer, currently sports a Zacks Rank of 1. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Abercrombie & Fitch’s current financial-year sales and EPS suggests growth of 3.4% and 736%, respectively, from the year-ago reported figures. ANF has delivered an earnings surprise of 480.6% in the last four quarters.

Boot Barn, a fashion retailer of apparel and accessories, currently sports a Zacks Rank of 1. The company has a trailing four-quarter earnings surprise of 13.5%, on average.

The Zacks Consensus Estimate for Boot Barn’s current financial-year sales suggests growth of 5.1% from the year-ago reported figure.

American Eagle Outfitters, a retailer of casual apparel, accessories and footwear, currently carries a Zacks Rank #2 (Buy). AEO has delivered an average earnings surprise of 9.2% in the last four quarters.

The Zacks Consensus Estimate for American Eagle Outfitters’ current financial-year EPS suggests growth of 7.2% from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

Urban Outfitters, Inc. (URBN) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report