Verizon: Too Much Debt to Be a Bargain

Verizon Communications Inc. (NYSE:VZ) is one of the largest providers of wireless communication services, broadband internet and entertainment services in the world. Unfortunately, in terms of its stock, it is now firmly an income only trade at best, and even income is in question given the high debt burden. Maybe the company can figure out how to use artificial intelligence to make the customer experience better or offer some new technology service that subscribers want, but that's currently not in the cards.

The company generates a staggering $1.16 million per employee in top line revenue and over $180,000 per employee in profits after tax. There is no doubt in my mind that Verizon will still be around in 20 years, still offering communication services. The question for investors is, how valuable will its stock price be? Despite the strength of the company itself, I think the stock's paper undervaluation is well deserved; here's why.

Verizon has a lot of competitive advantages

Verizon has been built nearly entirely via internal growth since its founding in the late 1990s as a joint venture with Vodafone (NASDAQ:VOD) with the acquisition of Alltel in 2009 still as the only major deal in its history, accounting for most of its goodwill. The company has several competitive advantages that have helped it maintain its position as one of the leading telecommunications companies in the U.S., which are outlined below.

Network Quality and Coverage: Verizon has consistently been recognized for the quality and reliability of its wireless network. The company has invested heavily in its infrastructure to ensure wide coverage and high-quality service for its customers. This has helped Verizon maintain a strong reputation and attract customers who prioritize network performance.

Strong Brand Recognition: Verizon enjoys strong brand recognition and a solid reputation in the telecommunications industry. This brand equity helps attract new customers and retain existing ones, providing a strong foundation for the company's continued success.

Business Customer Base: Verizon has a strong presence in the business and government sectors, providing services such as IoT, managed network services and cloud solutions. This customer base can contribute to more stable revenue streams and less vulnerability to consumer market fluctuations.

Early Adoption of 5G Technology: Verizon has been proactive in adopting and deploying 5G technology, securing valuable spectrum licenses and investing in infrastructure to support the new network. As a result, the company has been able to establish itself as a leader in 5G, which could potentially provide a competitive edge as the technology becomes more widely adopted.

Diverse Service Offerings: Verizon's broad range of services, including wireless and wireline communication services, entertainment, IoT, cloud and security, help it cater to a wide variety of customers. This diversification can contribute to the company's stability and growth.

Scale and Market Share: As one of the largest telecommunications companies in the U.S., Verizon benefits from economies of scale, which can lead to cost savings and operational efficiencies. Additionally, the company's significant market share allows it to exert influence over suppliers and partners, potentially leading to more favorable terms and partnerships.

Debt burden is weighing on Verizon's shares

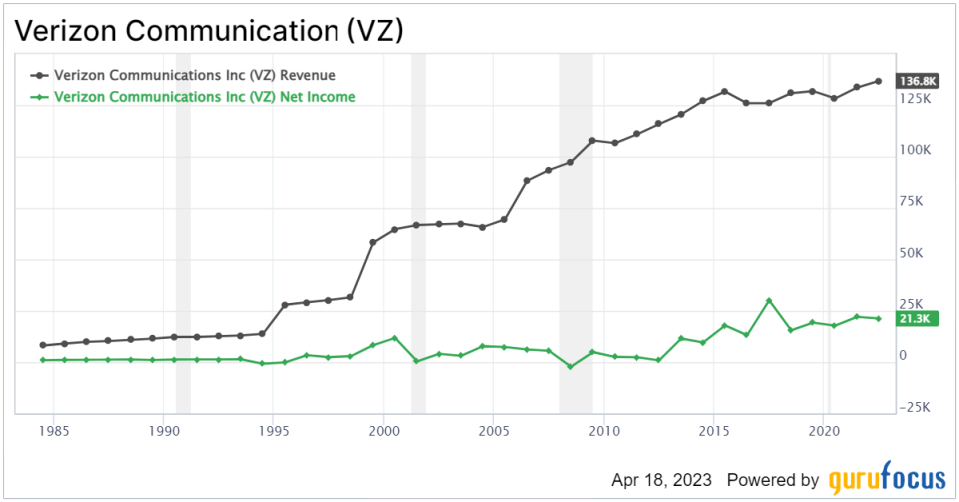

With the U.S. telecom market mostly having reached the saturation point, Verizon's growth has been slow on the top line, but the company has squeezed a lot of profit out on the bottom line by keeping its operating costs pretty level for the last decade. This has helped it book over $175 billion in total net income since 2013.

To do this, however, Verizon had to increase its long-term debt from $89 billion to over $143 billion - not an insignificant amount. So, despite retained earnings skyrocketing from just under $2 billion in 2013 to over $82 billion currently, that hasnt translated into any additional market value. The only silver lining is that on all of its debt, now totally $181 billion, Verizon only pays around $3.6 billion in interest expenses.

Past results don't mean anything for the future

Just because Verizon's stock price has been dead money for years does not mean it will continue to be that way. Verizon generates plenty of cash to cover its dividend and continue to grow.

In January, the company reported a 3.5% year-over-year increase in sales to $35.3 billion for the fourth quarter, which translated to growth of 2.4% annualized, beating estimates by $160 million. Its wireless service experienced better results, with a 5.9% increase for the quarter and 8.6% for the year. The adjusted Ebitda of $11.7 billion boasts an impressive 33.3% adjusted Ebitda margin, although the adjusted earnings per share of $1.19 was down by 10.5% year over year. Verizon also generated $14.1 billion in free cash flow (FCF) for the year after accounting for interest expenses, resulting in a 9% FCF yield that sufficiently covered its 6.9% dividend yield.

Verizon expects growth to continue this year with an estimate of 3.5% growth in its wireless service and $47.5 to $48 billion in adjusted Ebitda. Factoring in an effective tax rate of roughly 23%, the company expects to earn $4.70 per share, which puts the forward price-earnings ratio at about 8.

Conclusion

Maybe Im wrong and Verizon's massive debt isnt a big deal at all. Everyone else in the industry takes on massive debt levels too. Thats the price of growing a communications company like this; it's a capital intensive business. In the short term, I think the stock seems oversold and could rebound back to the levels it saw at the end of 2022. However, I dont think there is any such thing as a "value price" for a company that can't report decent growth, no matter how sweet the dividend may be.

This article first appeared on GuruFocus.