Vermilion Energy's (TSE:VET) Upcoming Dividend Will Be Larger Than Last Year's

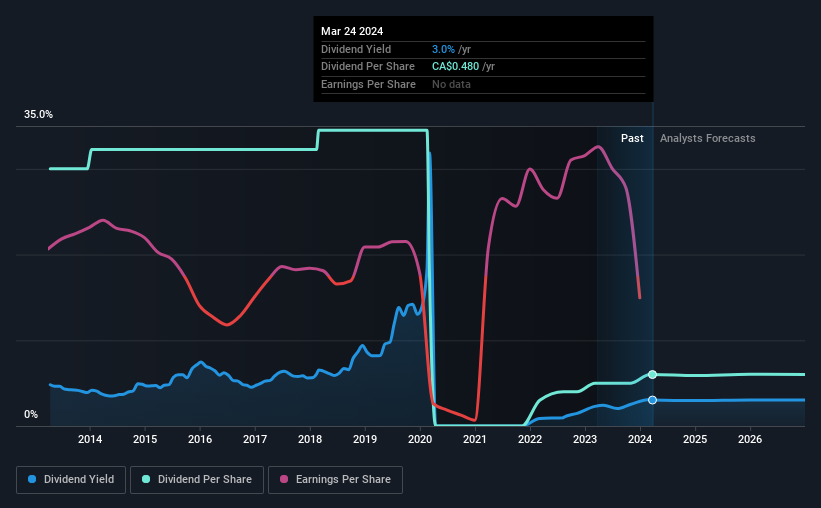

Vermilion Energy Inc. (TSE:VET) has announced that it will be increasing its dividend from last year's comparable payment on the 15th of April to CA$0.12. This takes the annual payment to 3.0% of the current stock price, which unfortunately is below what the industry is paying.

View our latest analysis for Vermilion Energy

Vermilion Energy's Earnings Easily Cover The Distributions

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. Vermilion Energy is not generating a profit, but its free cash flows easily cover the dividend, leaving plenty for reinvestment in the business. We generally think that cash flow is more important than accounting measures of profit, so we are fairly comfortable with the dividend at this level.

Over the next year, EPS is forecast to expand by 157.0%. If the dividend continues on this path, the payout ratio could be 43% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2014, the dividend has gone from CA$2.40 total annually to CA$0.48. The dividend has fallen 80% over that period. A company that decreases its dividend over time generally isn't what we are looking for.

The Company Could Face Some Challenges Growing The Dividend

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. We are encouraged to see that Vermilion Energy has grown earnings per share at 34% per year over the past five years. Even though the company is not profitable, it is growing at a solid clip. If the company can turn a profit relatively soon, we can see this becoming a reliable income stock.

Our Thoughts On Vermilion Energy's Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 2 warning signs for Vermilion Energy that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.