Visa Stock (NYSE:V): Is Its Growth Slowdown Cause for Concern?

Visa (NYSE:V) recently posted its Q1-2024 results, with revenue growth implying a notable slowdown in the business. The card payments processor giant grew its top line by roughly 9%, marking the worst growth rate in the past 2.5 years. While this could be a cause for concern, viewing this in perspective is essential. In fact, with anticipated acceleration in growth in the second half of 2024, this will likely be another exciting year for Visa. Thus, my outlook on Visa stock remains bullish.

Is Visa’s Revenue Growth Actually Slowing Down?

Visa’s Q4 results continued a trend that has persisted for several quarters now – that of decelerating revenue growth. Take a look at the company’s revenue growth over the past eight quarters:

Q4-2020: 28.6%

Q1:2021: 24.1%

Q2-2021: 25.5%

Q3-2021: 18.7%

Q4-2021: 18.7%

Q1-2022: 12.4%

Q2-2023: 11.1%

Q3-2023: 11.7%

Q4-2023 10.5%

Q1-2024: 8.8%

Visa’s revenue deceleration appears to have formed a clear trend over the past 2.5 years. However, it’s crucial to interpret these numbers in the context of Visa’s overall growth trajectory, which hasn’t been slowing down but rather normalizing. The remarkable 20%+ growth rates observed in 2020-21 were inflated due to a substantial post-pandemic surge in consumer spending, which has since subsided.

Now that a full normalization is likely already underway, we can anticipate Visa’s growth returning to its historical mean, hovering in the low double-digits. Although the 8.8% revenue growth to $8.6 billion in Q1 might signal a potential shift in the wrong direction, I remain optimistic about a quick rebound in Visa’s growth.

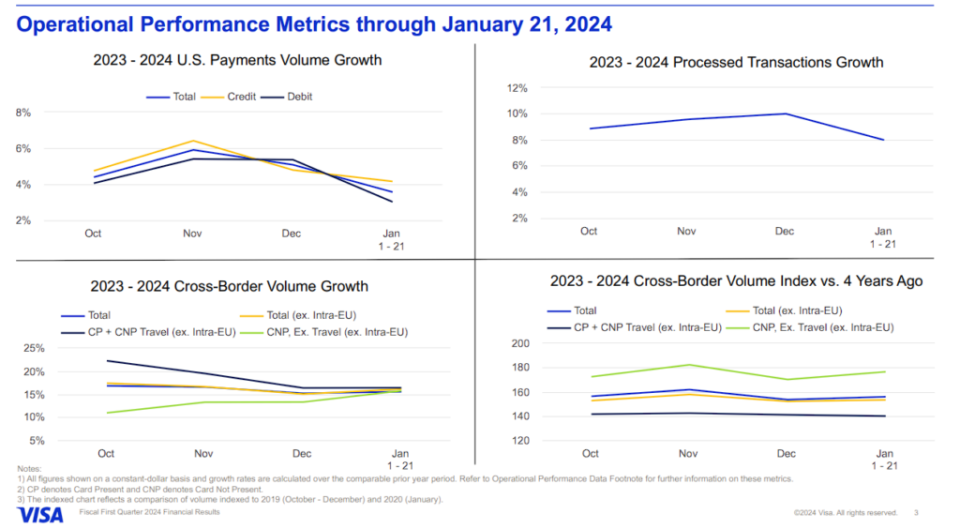

The most recent quarter’s dip can be attributed to a temporary slowdown in U.S. spending during October, leading to a modest 5% increase in domestic (U.S.) payment volumes. However, management has indicated a rebound in growth during November and December, suggesting that these challenges are primarily of cyclical nature.

Considering the positive indicators in the U.S. economy, such as declining inflation and robust unemployment rates, coupled with the possibility of interest rate cuts later in the year, there’s a high likelihood of a resurgence in payment volumes. Meanwhile, international growth remains robust and is poised to contribute to Visa’s overall double-digit growth. Notably, Visa achieved a strong increase of 11% in total payment volume internationally.

The company also benefits from a strong tailwind in cross-border payments volumes driven by the thriving travel industry. Total cross-border volume witnessed a significant 16% year-over-year boost, with a remarkable 19% increase in cross-border travel-related spending.

While one might argue that this growth is a post-pandemic recovery phenomenon, the data suggests otherwise. The post-COVID recovery has already occurred, and the current figures indicate sustained high levels of spending on travel. Notably, back in Q4, Visa’s cross-border travel volume index reached 139% compared to 2019, and this trend continued into Q1, with the index increasing to 142%.

Visa’s management team seems to expect a rebound in revenue growth as well. For Fiscal 2024, it expects low double-digit revenue growth, suggesting a reacceleration, likely in the second half of the year.

Strong Buybacks to Drive Mid-Teens EPS Growth in FY2024

Visa’s optimistic growth outlook and impressive free cash flow generation have empowered the company to buy back stock consistently, which is expected to bolster EPS growth in the mid-teens this year, as per management’s guidance.

As of the end of Q1, Visa’s Class A share count had decreased to 1.58 million, down 3% compared to the previous year. The synergy of sustained low double-digit revenue growth, coupled with the added impact of ongoing share repurchases on per-share metrics, is poised to propel EPS growth to approximately 13% based on Wall Street’s forecasts. Thus, EPS for the year is expected to land at $9.92.

My confidence in Visa’s performance goes beyond just meeting Wall Street’s estimates. I believe the company is positioned to surpass them. Even if reality ends up aligning with expectations, though, Fiscal 2024 promises to be another year characterized by outstanding double-digit growth, a testament to Visa’s enduring trend. This brings us to its valuation. Is the stock’s extended rally justified based on these estimates?

Is Visa Stock Overvalued After Its Recent Gains?

Visa stock has rallied by about 21% over the past year, reaching new all-time highs by the week lately. At its current levels, the stock’s P/E stands at about 27.9, which certainly implies a premium even for a company growing in the double-digits. Nevertheless, Visa stock has always been relatively expensive and is likely to continue to be so.

Investors value its one-of-a-kind moat inherent to its business model and the advantages of operating essentially in a duopoly with Mastercard. It’s not uncommon for Visa to trade at 25x+ EPS, as its double-digit bottom-line growth has always managed to catch up to these multiples eventually. Thus, I would consider Visa fairly valued, retaining the prospect of upside.

Is V Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Visa features a Strong Buy consensus rating based on 22 Buys and two Holds assigned in the past three months. At $303.74, the average Visa stock price target implies 10.35% upside potential.

If you’re wondering which analyst you should follow if you want to buy and sell Visa stock, the most accurate analyst covering the stock (on a one-year timeframe) is Sanjay Sakhrani from KBW, boasting an average return of 20.77% per rating and a 100% success rate.

The Takeaway

To sum up, while Visa’s recent Q1-2024 results revealed a temporary slowdown in revenue growth, it’s essential to contextualize this within the broader normalization of the company’s trajectory. What appears to be a consistent deceleration over the past 2.5 years aligns with the end of the post-pandemic surge in consumer spending (expansion) and subsequent rise in interest rates (contraction).

Despite the slight dip in Q1 in U.S. payment volumes, optimistic indicators in the U.S. economy and solid international growth position the company for a rebound in the latter half of 2024. With EPS growth set to hover again in the mid-teens, I remain bullish on Visa stock despite its seemingly hefty valuation.