Vita Coco (NASDAQ:COCO) Surprises With Strong Q4, Stock Jumps 10.3%

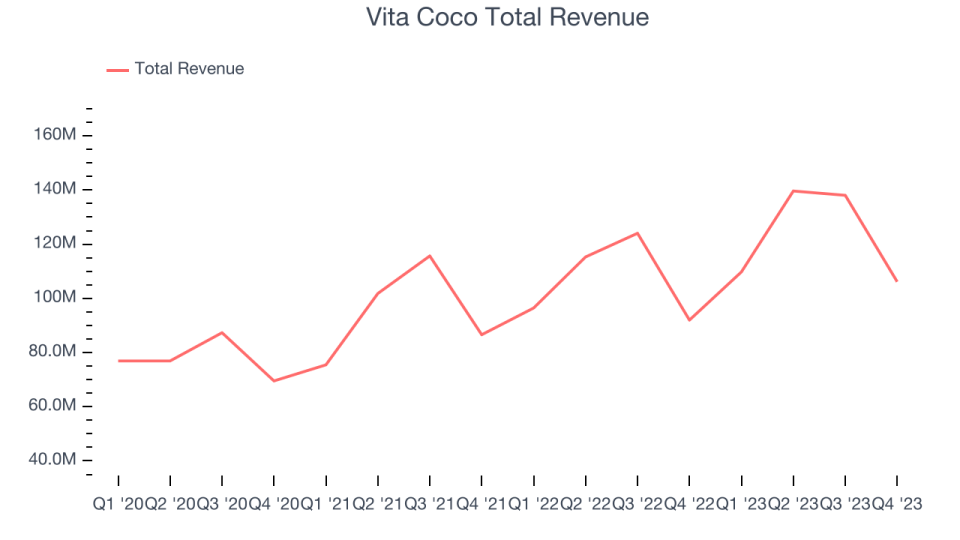

Coconut water company The Vita Coco Company (NASDAQ:COCO) reported results ahead of analysts' expectations in Q4 FY2023, with revenue up 15.4% year on year to $106.1 million. On the other hand, the company's full-year revenue guidance of $500 million at the midpoint came in slightly below analysts' estimates. It made a GAAP profit of $0.11 per share, improving from its profit of $0.03 per share in the same quarter last year.

Is now the time to buy Vita Coco? Find out by accessing our full research report, it's free.

Vita Coco (COCO) Q4 FY2023 Highlights:

Revenue: $106.1 million vs analyst estimates of $99.23 million (7% beat)

EPS: $0.11 vs analyst estimates of $0.07 ($0.04 beat)

Management's revenue guidance for the upcoming financial year 2024 is $500 million at the midpoint, missing analyst estimates by 0.7% and implying 1.3% growth (vs 15.4% in FY2023)

However, management's adjusted EBITDA guidance for the upcoming financial year 2024 is $76 million at the midpoint, above analyst estimates of $74 million

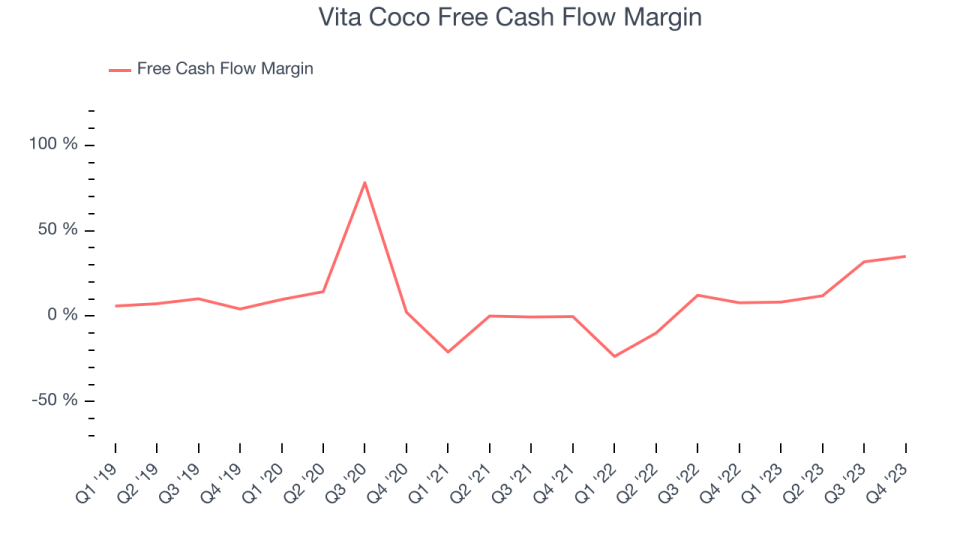

Free Cash Flow of $37.09 million, down 15.5% from the previous quarter

Gross Margin (GAAP): 37.5%, up from 24.4% in the same quarter last year

Sales Volumes were up 3% year on year

Market Capitalization: $1.27 billion

Martin Roper, the Company’s Chief Executive Officer, said, “We are extremely pleased with this year's results with 15% net sales growth, Net Income of $47 million, and Adjusted EBITDA1 of $68 million, which were all at the high end of our expectations. The coconut water category is healthy and our team continues to deliver strong results across our major markets as we gain branded share and benefit from our private label coconut water supply relationships. We expect our full year 2024 net sales to be between $495 and $505 million, driven by healthy coconut water volume growth, offset by the loss of some of our private label coconut oil business. While the macro environment remains very dynamic, we expect 2024 Adjusted EBITDA2 to be between $74 and $78 million. We remain focused on driving long term growth of the coconut water category and our brands.”

Founded in 2004 followed by a 2021 IPO, The Vita Coco Company (NASDAQ:COCO) offers coconut water products that are a natural way to quench thirst.

Beverages and Alcohol

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the explosion of alcoholic craft beer drinks or the steady decline of non-alcoholic sugary sodas. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Sales Growth

Vita Coco is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

As you can see below, the company's annualized revenue growth rate of 16.7% over the last three years was impressive for a consumer staples business.

This quarter, Vita Coco reported robust year-on-year revenue growth of 15.4%, and its $106.1 million in revenue exceeded Wall Street's estimates by 7%. Looking ahead, Wall Street expects sales to grow 2.2% over the next 12 months, a deceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Vita Coco's free cash flow came in at $37.09 million in Q4, up 417% year on year. This result represents a 34.9% margin.

Over the last two years, Vita Coco has shown strong cash profitability, giving it an edge over its competitors and the option to reinvest or return capital to investors while keeping cash on hand for emergencies. The company's free cash flow margin has averaged 10.3%, quite impressive for a consumer staples business. Furthermore, its margin has averaged year-on-year increases of 24.4 percentage points over the last 12 months. Shareholders should be excited as this will certainly help Vita Coco achieve its strategic long-term plans.

Key Takeaways from Vita Coco's Q4 Results

We were impressed by how significantly Vita Coco blew past analysts' EPS expectations this quarter. We were also excited its revenue outperformed Wall Street's estimates. On the other hand, its full-year revenue guidance was underwhelming. However, adjusted EBITDA guidance came in ahead, which is sure to blunt the impact of the below-Consensus revenue guidance. Overall, we think this was a strong quarter that should satisfy shareholders. The stock is up 9.9% after reporting and currently trades at $24.66 per share.

Vita Coco may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.