W.W. Grainger (GWW): Modestly Overvalued or a Hidden Gem?

W.W. Grainger Inc's (NYSE:GWW) stock experienced a daily loss of -0.84%, culminating in a 3-month gain of 6.37%. With an Earnings Per Share (EPS) of 34.7, the question arises: is the stock modestly overvalued? This article aims to answer this question through a comprehensive valuation analysis. Read on to gain a deeper understanding of W.W. Grainger's intrinsic value.

Company Snapshot

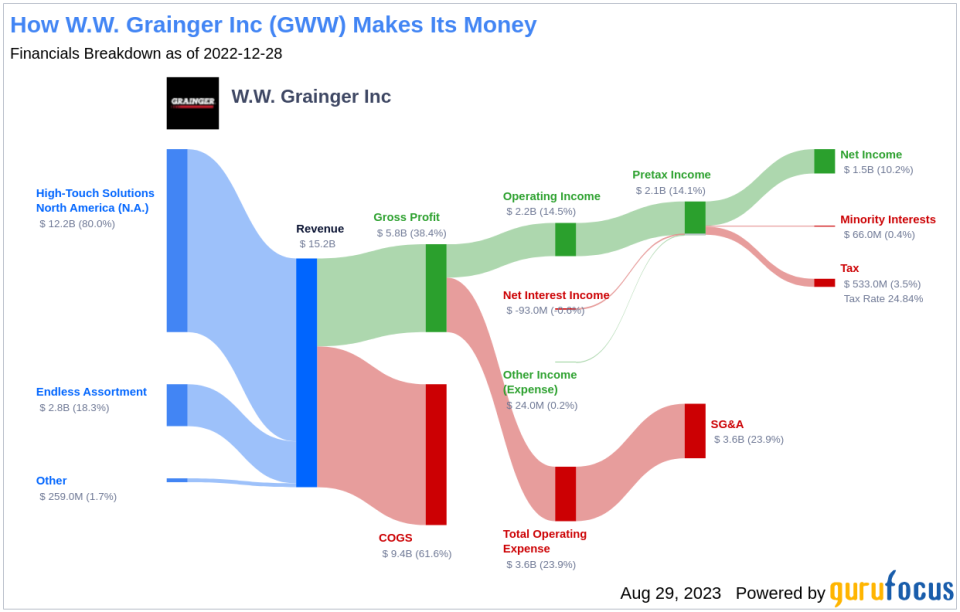

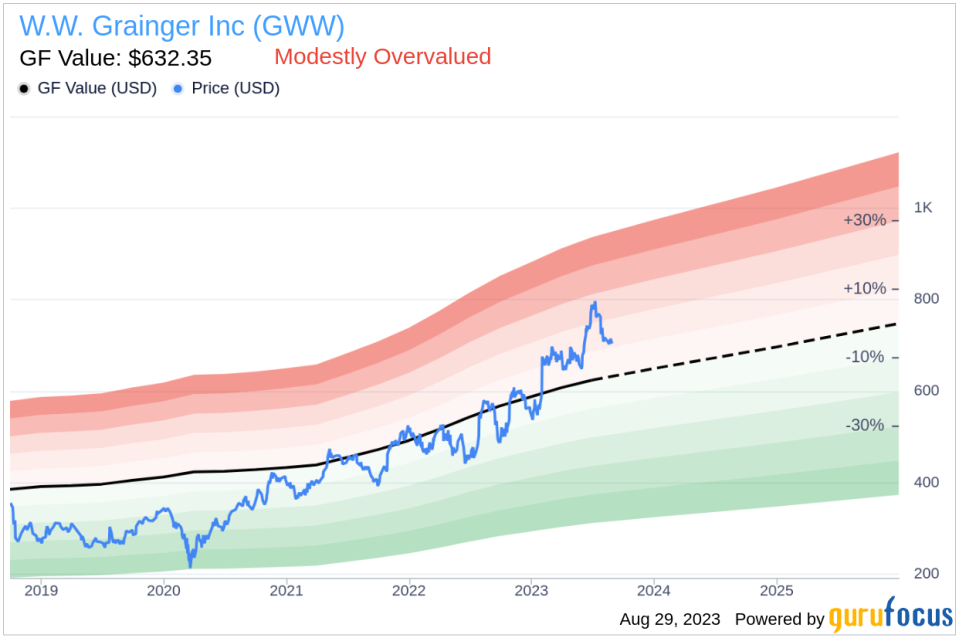

W.W. Grainger Inc operates as a leading distributor of maintenance, repair, and operating products, sourcing from over 4,500 suppliers. The company caters to approximately 5 million customers through various platforms, including online and electronic purchasing platforms, vending machines, catalog distribution, and a network of over 300 global branches. Over the years, W.W. Grainger has significantly invested in its e-commerce capabilities, ranking as the 11th-largest e-retailer in North America. Despite a current stock price of $704.22, the company's fair value, or GF Value, stands at $632.35, suggesting a potential overvaluation.

Understanding GF Value

The GF Value is a proprietary measure that represents the intrinsic value of a stock. It is derived from three key factors: historical multiples at which the stock has traded, an internal adjustment based on the company's past returns and growth, and future business performance estimates. The GF Value Line indicates the fair value at which the stock should ideally trade. If the stock price is significantly above the GF Value Line, it is potentially overvalued, leading to poor future returns. Conversely, if it is significantly below the GF Value Line, the stock may be undervalued, signaling potentially high future returns.

According to GuruFocus' valuation method, W.W. Grainger's stock, with its current market cap of $35.20 billion, is considered modestly overvalued. This suggests that the long-term return of its stock is likely to be lower than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Assessing Financial Strength

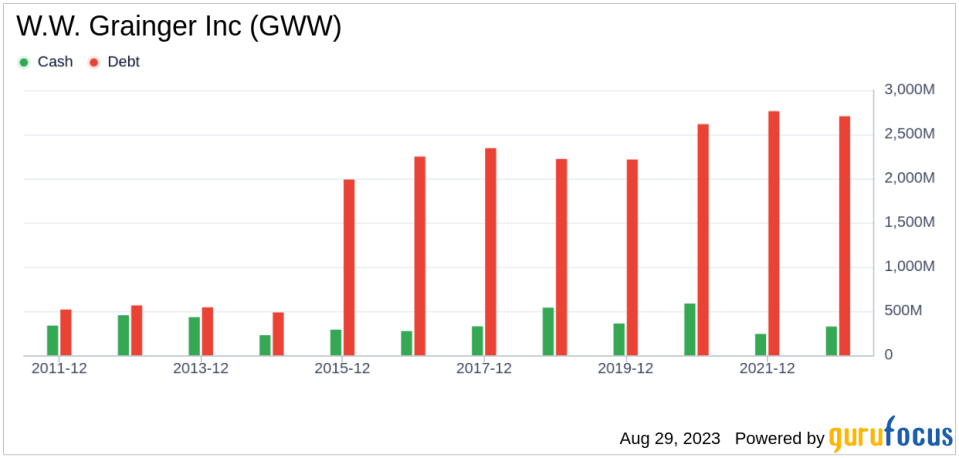

Companies with poor financial strength pose a high risk of permanent capital loss to investors. To avoid this, it is crucial to thoroughly research and review a company's financial strength before purchasing shares. Factors like the cash-to-debt ratio and interest coverage can offer valuable insights into a company's financial strength. W.W. Grainger's cash-to-debt ratio of 0.19 ranks worse than 65.52% of 145 companies in the Industrial Distribution industry. However, the company's overall financial strength is 7 out of 10, indicating fair financial health.

Profitability and Growth

Investing in profitable companies carries less risk, especially if the companies have demonstrated consistent profitability over a long period. W.W. Grainger has been profitable for 10 years over the past decade. With revenues of $16 billion and Earnings Per Share (EPS) of $34.7 in the past 12 months, the company's operating margin of 15.53% is better than 93.29% of 149 companies in the Industrial Distribution industry. GuruFocus ranks W.W. Grainger's profitability as strong.

Growth is a significant factor in a company's valuation. A faster-growing company creates more value for shareholders, especially if the growth is profitable. W.W. Grainger's 3-year average annual revenue growth is 12.5%, ranking better than 68.97% of 145 companies in the Industrial Distribution industry. The 3-year average EBITDA growth rate is 20.3%, ranking better than 63.08% of 130 companies in the same industry.

ROIC vs WACC

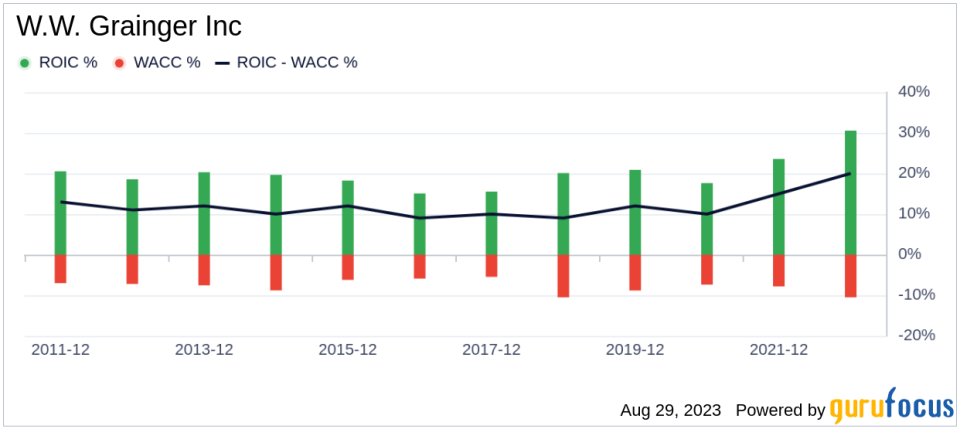

Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. For the past 12 months, W.W. Grainger's ROIC is 33.36, and its WACC is 11.32, indicating a higher return on invested capital than the cost of capital.

Conclusion

In summary, W.W. Grainger's (NYSE:GWW) stock appears to be modestly overvalued. The company's financial condition is fair, and its profitability is strong. Its growth ranks better than 63.08% of 130 companies in the Industrial Distribution industry. To learn more about W.W. Grainger's stock, check out its 30-Year Financials here.

To discover high-quality companies that may deliver above-average returns, check out the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.