Walmart (WMT) Is Marching Ahead of the Industry: Here's Why

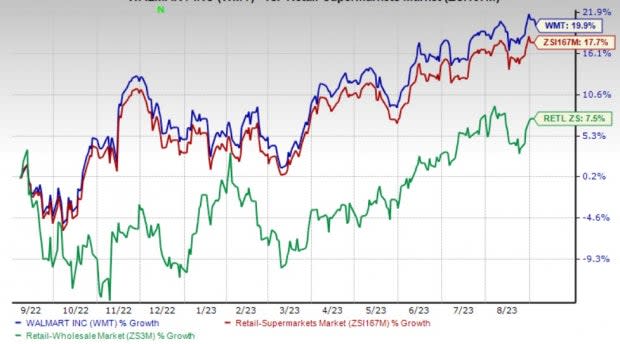

Walmart Inc. WMT enjoys a favorable position as its shares rose close to 20% in the past year compared with the industry’s growth of 17.6%. The supermarket giant has also outperformed the Zacks Retail – Wholesale sector’s growth of 7.5% in the same time frame. Walmart’s unparalleled efforts to boost omnichannel efforts and upgrade customer experience are a major reason behind its growth story.

Over a sustained period, this Zacks Rank #2 (Buy) company has achieved consecutive growth in comp sales, thanks to its remarkable performance in both brick-and-mortar stores and digital platforms. We believe that these upsides keep Walmart well-placed for continued gains. The Zacks Consensus Estimate for the current fiscal year EPS has jumped from $6.22 to $6.42 in the past 30 days.

E-commerce - A Significant Driving Force

Walmart's e-commerce operations have been expanding. During the second quarter, e-commerce net sales accounted for 15% of the company's total net sales. The company has been actively pursuing numerous e-commerce initiatives, which encompass acquisitions, partnerships, and enhancements to delivery and payment systems.

The company is also making innovations in its supply chain, increasing capacity, and establishing new ventures such as Walmart GoLocal, Walmart Connect, Walmart Luminate, Walmart+, Spark Delivery, Marketplace, and Walmart Fulfillment Services. In the second quarter of fiscal 2024, global e-commerce sales saw an impressive 24% increase, driven by the strength of its omnichannel capabilities, including pickup and delivery services.

Within the United States, e-commerce sales jumped 24%, largely propelled by the robust performance of pickup and delivery services as well as advertising efforts. The International segment experienced a 26% increase in e-commerce sales, primarily due to the strength of store-fulfilled orders. At Sam's Club, e-commerce sales witnessed 18% growth, largely attributed to the solid performance of curbside pickup services.

Image Source: Zacks Investment Research

Enhancing Delivery Services

Walmart has made significant strides in strengthening its delivery capabilities, evident through various strategic moves. These include partnering with Salesforce, expanding its InHome delivery service, investing in DroneUp, launching the Walmart+ membership program, and conducting a pilot program with Cruise to explore grocery delivery using self-driving electric vehicles.

Prior to these initiatives, Walmart introduced Express Delivery in April 2021 and formed partnerships with Point Pickup, Skipcart, AxleHire, and Roadie in January 2019. Additionally, the acquisition of Parcel in September 2017 was a key strategic move to enhance its delivery services. Additionally, Walmart offers store and curbside pickup options. As of the second quarter of fiscal 2024, Walmart U.S. had nearly 4,600 pickup locations and more than 4,000 same-day delivery stores. As of Jan 31, 2023, the company had more than 8,100 pickups and nearly 7,000 delivery locations globally.

Walmart Inc. Price, Consensus and EPS Surprise

Walmart Inc. price-consensus-eps-surprise-chart | Walmart Inc. Quote

Splendid Comp Sales

Strong e-commerce business, combined with unmatched store operations, has been contributing to Walmart’s comp sales. The company has been paying attention to renovating stores, enhancing product offerings and undertaking in-store and digital advancements. WMT remodeled 165 U.S. stores in the second quarter of fiscal 2024.

Walmart's effective pricing strategy has also proven advantageous, playing a pivotal role in attracting and retaining customers. U.S. comp sales, excluding fuel, improved 6.4% in the second quarter. The segment experienced gains from grocery and health & wellness. Moreover, e-commerce boosted comps by 230 basis points (bps). Sam’s Club’s comp sales, excluding fuel, grew 5.5%. Comp sales saw strength across most categories, mainly led by food and consumables and healthcare.

A Look Ahead

For fiscal 2024, Walmart expects consolidated net sales growth of 4-4.5% at constant currency (cc). Management expects the consolidated operating income to increase roughly 7-7.5% at cc, including a 30 bps positive impact of LIFO. Management envisions adjusted EPS in the band of $6.36-$6.46, suggesting growth from $6.29 recorded in fiscal 2023.

Other Solid Picks

Here, we have highlighted three other top-ranked stocks.

Dillard's, Inc. DDS, a department store retailer, currently sports a Zacks Rank #1 (Strong Buy). DDS has a trailing four-quarter negative earnings surprise of 77.1%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Dillard's third-quarter EPS has increased from $6.66 to $7.04 in the past 30 days.

Ross Stores ROST currently carries a Zacks Rank #2. This off-price retailer has an expected EPS growth rate of 11.6% for three to five years.

The Zacks Consensus Estimate for Ross Stores’ current financial-year EPS suggests growth of 19.4% from the year-ago reported figure. ROST has a trailing four-quarter earnings surprise of 11.4%, on average.

Build-A-Bear Workshop, Inc. BBW has a trailing four-quarter earnings surprise of 21.6%, on average. BBW, which is a multi-channel retailer of plush animals and related products, holds a Zacks Rank #2 at present.

The Zacks Consensus Estimate for Build-A-Bear Workshop’s current financial-year EPS suggests growth of 14.3% from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dillard's, Inc. (DDS) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

Ross Stores, Inc. (ROST) : Free Stock Analysis Report

Build-A-Bear Workshop, Inc. (BBW) : Free Stock Analysis Report