Wayfair's (NYSE:W) Q4 Earnings Results: Revenue In Line With Expectations

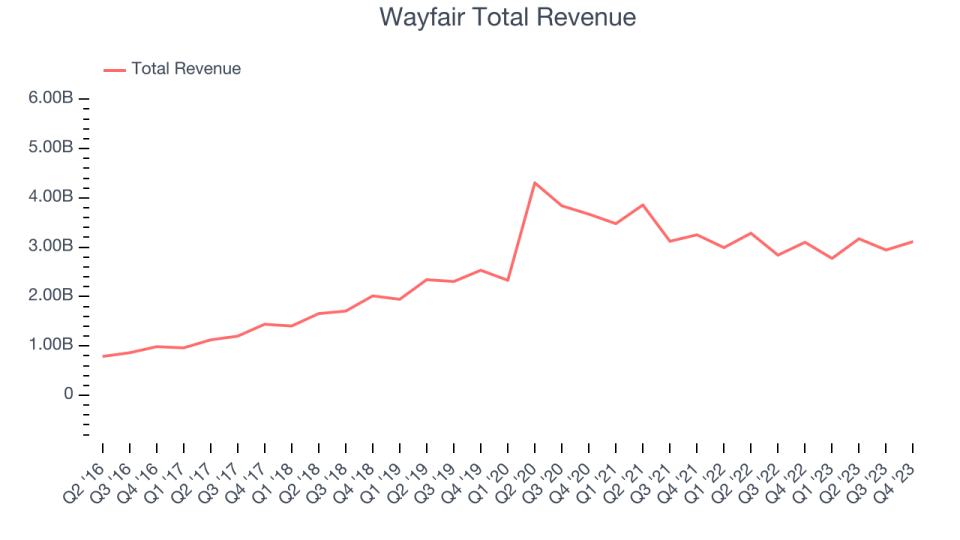

Online home goods retailer Wayfair (NYSE: W) reported results in line with analysts' expectations in Q4 FY2023, with revenue flat year on year at $3.11 billion. It made a non-GAAP loss of $0.11 per share, improving from its loss of $1.70 per share in the same quarter last year.

Is now the time to buy Wayfair? Find out by accessing our full research report, it's free.

Wayfair (W) Q4 FY2023 Highlights:

Revenue: $3.11 billion vs analyst estimates of $3.11 billion (small beat)

EPS (non-GAAP): -$0.11 vs analyst estimates of -$0.15

Free Cash Flow of $62 million, up 47.6% from the previous quarter

Gross Margin (GAAP): 30.3%, up from 28.8% in the same quarter last year

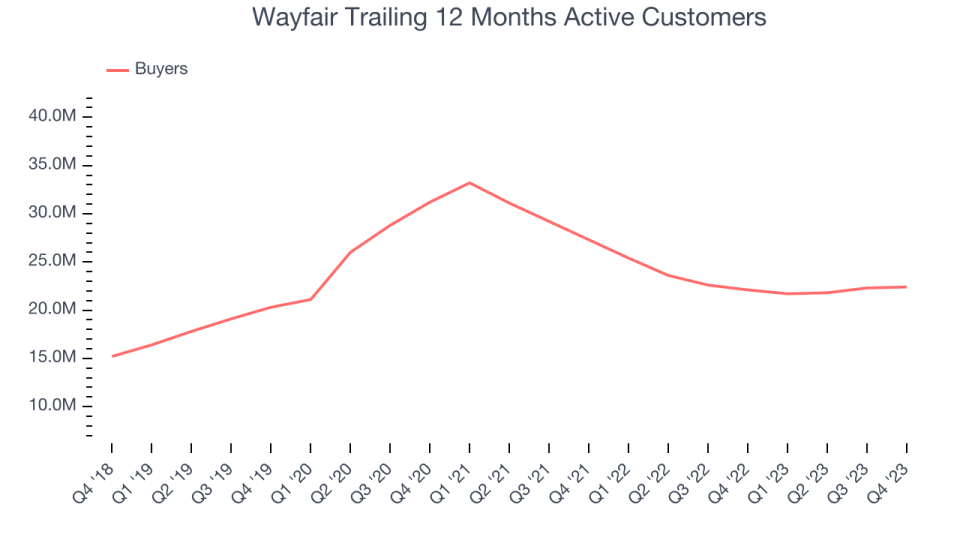

Trailing 12 Months Active Customers: 22.4 million, up 300,000 year on year

Market Capitalization: $5.75 billion

Launched in 2002 by founder Niraj Shah, Wayfair (NYSE: W) is a leading online retailer for mass market home goods in the US, UK, Canada, and Germany.

Online Retail

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Sales Growth

Wayfair's revenue has been declining over the last three years, dropping on average by 3.4% annually. This quarter, Wayfair reported lacklustre 0.4% year-on-year revenue growth, in line with analysts' expectations.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Usage Growth

As an online retailer, Wayfair generates revenue growth by expanding its number of buyers and the average order size in dollars.

Wayfair has been struggling to grow its active buyers, a key performance metric for the company. Over the last two years, its buyers have declined 13.9% annually to 22.4 million. This is one of the lowest rates of growth in the consumer internet sector.

Luckily, Wayfair added 300,000 active buyers in Q4, leading to 1.4% year-on-year growth.

Revenue Per Buyer

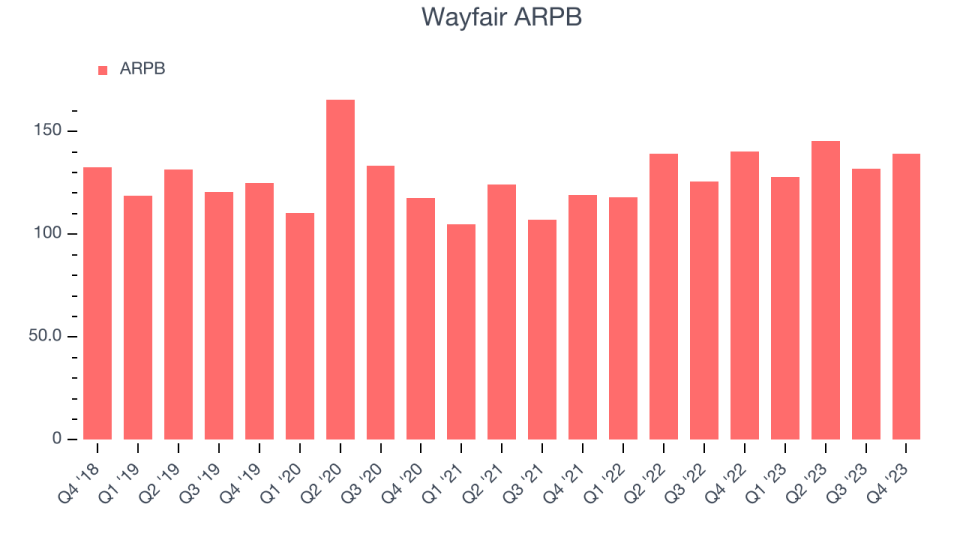

Average revenue per buyer (ARPB) is a critical metric to track for consumer internet businesses like Wayfair because it measures how much customers spend per order.

Wayfair's ARPB growth has been strong over the last two years, averaging 9.6%. Although its active buyers have shrunk during this time, the company's ability to successfully increase prices demonstrates its platform's enduring value for existing buyers. This quarter, ARPB declined 0.9% year on year to $139.02 per buyer.

Key Takeaways from Wayfair's Q4 Results

We struggled to find many strong positives in these results. Its revenue growth regrettably slowed as management called out a difficult macro environment. The company is exercising efficiency, however, as its free cash flow of $62 million beat analysts' estimates of break-even cash profitability. Overall, the results could have been better. The stock is up 3.6% after reporting and currently trades at $50.5 per share.

So should you invest in Wayfair right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.