Why bearish arguments sound better than bullish arguments

In the world of investment writing, there is a large and perpetual stream of content focused on why we are at or near a peak in the stock market.

The top callers, the permabears, or whatever you want to call those who call for lower stock prices (and often higher precious metals prices), get to sound smart because their view on the market is not open-ended, but closed.

Unlike those who think the bull market will continue, those calling for an end include all the elements of a story — exposition, rising action, a climax, a future falling action, and an ending.

And while stories are an integral part of all market forecasting and discussion, rarely do bull-case narratives get past the rising action — beyond that, the bulls are left to fill in their own blanks. Bears do that work for you.

And with a complete story in hand, bear theses also offer the guise of “cutting through the noise” that many a bull case assumes will be taken in stride. Or as Morgan Housel wrote last year, “In investing, a bull sounds like a reckless cheerleader, while a bear sounds like a sharp mind who has dug past the headlines.”

Last month, influential investment manager Howard Marks made waves in markets when he wrote a memo that said, among other things, “Since we never know when risky behavior will bring on a market correction, I’m going to issue a warning today rather than wait until one is upon us.”

On its “Fast Money” program last night, CNBC ran a chyron asking, “Party like it’s 1999?”

And in the weeks that have followed Marks’ memo, it seems the dominant theme in markets — during an earnings season, mind you, that has seen S&P 500 companies report double-digit earnings growth for the second-straight quarter, the first time this has happened since 2011 — has been to beg this question.

Now, if stock prices are simply a reflection of how much investors are willing to pay for future earnings streams from companies, then reported earnings from America’s biggest companies ought not to really cause much angst. Additionally, the market’s overall rise since the end of the last recession looks quite tempered when compared to what we saw in the ’90s.

Additionally, in a report on ETF.com this weekend, Dave Nadig cited influential market commentator Barry Ritholtz who contends that the market rally since the March ’09 bottom is not when the current bull market began, but that this bull run began we broke to new highs in early 2013. By this measure, then, we’re only up about 60% since that break to new highs and the market’s rally then looks quite mediocre relative to history.

Yahoo Finance contributor Joe Fahmy also recently argued that everywhere you turn people are spinning bearish tales about the market, which is not a recipe for a market to fall out of bed.

“I’m not saying to never be cautious and to just blindly go long this market,” Fahmy writes. “I’m simply saying that it’s tough to see a prolonged correction when the majority of people are scared and expecting it.”

In a note to clients published Monday evening, the team at Bespoke Investment Group also took on this issue which has bubbled up in recent weeks. “The one thing that always comes to mind when we see a deluge of ‘bubble’ articles is that true bubbles aren’t accompanied by an almost consensus opinion that we’re in a bubble,” Bespoke writes.

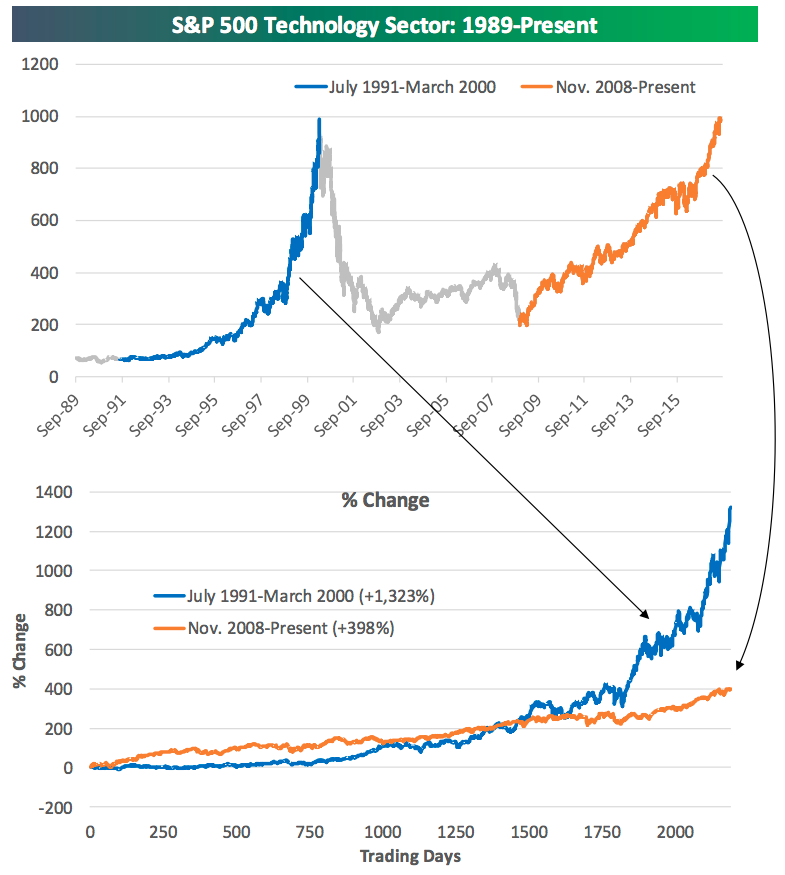

In its note, Bespoke includes a number of charts, but we think this one is most instructive, showing the points change in the S&P 500 tech sector through time and the percent change we saw during the ’90s vs. today. In short, it’s no contest — from the post-crisis lows this sector is up about 400%, while from July ’91 to March ’00, this index rose over 1,200%.

But in a world in which “The Big Short” is nominated for Oscars and everyone wants to say they too saw that trade coming, saying that we’re probably not going to see a market crash anytime soon can range from coming off naïve, to uncool, to downright ignorant depending on the critic.

And either way, it’s simply not as good of a story.

Which is why we’ll never stop hearing proposed answers to the question of whether this is the top.

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland

Read more from Myles here: