Wendy's (WEN) Stock Down on Q4 Earnings and Revenue Miss

The Wendy's Company WEN reported fourth-quarter fiscal 2023 results, with earnings and revenues missing the Zacks Consensus Estimate. On a year-over-year basis, the top line rose while the bottom line declined. Solid same-restaurant sales and strength in digital momentum aided the company’s performance.

Following the announcement, Wendy's shares declined 1.5% during the trading session on Feb 15.

In 2023, Wendy’s system saw robust growth in sales, profit and cash flow. This was fueled by progress on strategic growth pillars. It marked the 13th consecutive year of global same-restaurant sales growth, showcasing consistent execution and strong franchisee alignment. The company also witnessed boosted digital sales and opened nearly 250 new restaurants worldwide. Despite inflationary challenges, U.S. company-operated restaurant margins returned to pre-COVID levels.

Q4 Earnings & Revenues

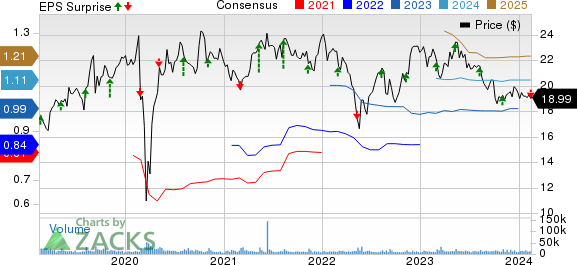

WEN reported adjusted earnings per share (EPS) of 21 cents, missing the Zacks Consensus Estimate by 8.7%. In the prior-year quarter, it reported adjusted EPS of 22 cents.

Revenues of $540.7 million missed the consensus mark of $546.6 million. However, the top line moved up 0.8% on a year-over-year basis on the back of higher same-restaurant sales. Also, a rise in franchise royalty revenues and advertising funds revenues added to the upside. This was partially offset by lower franchise rental income due to fewer lease assignments.

The Wendy's Company Price, Consensus and EPS Surprise

The Wendy's Company price-consensus-eps-surprise-chart | The Wendy's Company Quote

Same-restaurant sales at international restaurants (excluding Argentina) rose 4.3% year over year compared with 9.9% a year ago. Our estimate was 4.9%.

Comps at global restaurants inched up 1.3% year over year compared with 6.4% in the prior-year quarter. Comps in the United States registered a 0.9% year-over-year improvement compared with 5.9% in the year-ago quarter.

In the quarter under review, Wendy’s inaugurated 94 restaurants globally, reflecting an increase of 74 net new units.

System-Wide Sales Discussion

During the reported quarter, global system-wide sales — including company-operated and franchise restaurants — rose 3.2% year over year. System-wide sales in the U.S. and International segments were up 2.3% and 9.7% year over year, respectively.

Operating Highlights

During the quarter under review, the company-operated restaurant margin came in at 13.5% compared with 15.1% in the prior-year quarter. The downside was due to higher commodity costs, declining customer counts and higher labor costs. This was partially offset by a higher average check.

General and administrative expenses were $65.7 million compared with $68.5 million a year ago. The downside was due to a decline in employee compensation and benefits. We suggested the metric to be $66.3 million.

Quarterly operating profit amounted to $86.6 million, up 3.1% from the year-ago levels. The positive trend was supported by increased franchise royalty revenues, a reduction in additional investment in breakfast advertising and a decline in general and administrative expenses. This was partially offset by a downtick in U.S. company-operated restaurant margins and higher amortization of cloud computing arrangement costs.

Net income was $46.9 million, up 13.6% from $41.3 million in the year-ago quarter.

Adjusted EBITDA totaled $126.6 million, up 2.5% from $123.5 million in the prior-year quarter. This was primarily backed by higher franchise royalty revenues, a reduction in additional investment in breakfast advertising and a decrease in general and administrative expenses. Our projection was $130.5 million.

Balance Sheet

Cash and cash equivalents as of Dec 31, 2023, totaled $516 million compared with $745.9 million on Jan 1, 2023. Inventories at the end of the fiscal fourth quarter amounted to $6.7 million compared with $7.1 million as of Jan 1, 2023. As of Dec 31, 2023, long-term debt was $2,732.8 million compared with $2,822.2 million at the end of Jan 1, 2023.

Management declared a quarterly dividend of 25 cents per share. The dividend will be paid out on Mar 15, 2024, to shareholders on record as of Mar 1, 2024.

2023 Highlights

Total revenues in 2023 amounted to $2,181.6 million compared with $2,095.5 million in 2022.

Adjusted EBITDA in 2023 came in at $535.9 million compared with $497.8 million in 2022.

In 2023, diluted EPS came in at 97 cents per share compared with 86 cents reported in the previous year.

2024 Outlook

For 2024, WEN expects global system-wide sales growth in the range of 5-6% compared with 6.1% reported in 2023. Adjusted EBITDA is projected in the band of $535-$545 million.

Adjusted EPS for 2024 is anticipated to be between $0.98 and $1.02.

The company suggests cash flow from operations in the band of $370-$390 million. Capital expenditures are envisioned to be between $90 million and $100 million. Free cash flow is forecasted in the range of $280-$290 million.

Zacks Rank

Wendy's currently has a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Recent Retail-Wholesale Releases

Restaurant Brands International, Inc. QSR reported fourth-quarter 2023 results, with earnings and revenues beating the Zacks Consensus Estimate. The top and the bottom line increased on a year-over-year basis.

The management cited concerns about an uncertain operating environment because of inflationary pressures, foreign exchange volatility, rising interest rates and general softening in the consumer environment (impacted by the conflict in the Middle East).

YUM! Brands, Inc. YUM reported drab fourth-quarter 2023 results, with earnings and revenues missing the Zacks Consensus Estimate. Revenues missed the consensus estimate for the third straight quarter.

Yum China Holdings, Inc. YUMC reported impressive fourth-quarter 2023 results, with earnings and revenues beating the Zacks Consensus Estimate. The top and the bottom line increased on a year-over-year basis.

YUMC achieved record-breaking revenues and profits and returned substantial value to shareholders through cash dividends and share repurchases. During the year, the company returned $833 million to shareholders, up 25% year over year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Yum! Brands, Inc. (YUM) : Free Stock Analysis Report

The Wendy's Company (WEN) : Free Stock Analysis Report

Restaurant Brands International Inc. (QSR) : Free Stock Analysis Report

Yum China (YUMC) : Free Stock Analysis Report