Is Weyerhaeuser Company's (NYSE:WY) Recent Performancer Underpinned By Weak Financials?

Weyerhaeuser (NYSE:WY) has had a rough three months with its share price down 36%. Given that stock prices are usually driven by a company’s fundamentals over the long term, which in this case look pretty weak, we decided to study the company's key financial indicators. In this article, we decided to focus on Weyerhaeuser's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for Weyerhaeuser

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Weyerhaeuser is:

4.5% = US$363m ÷ US$8.1b (Based on the trailing twelve months to March 2020).

The 'return' is the amount earned after tax over the last twelve months. Another way to think of that is that for every $1 worth of equity, the company was able to earn $0.04 in profit.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learnt that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Weyerhaeuser's Earnings Growth And 4.5% ROE

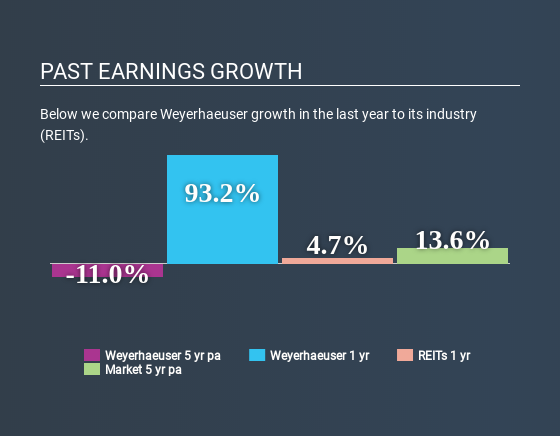

At first glance, Weyerhaeuser's ROE doesn't look very promising. A quick further study shows that the company's ROE doesn't compare favorably to the industry average of 5.8% either. Therefore, it might not be wrong to say that the five year net income decline of 11% seen by Weyerhaeuser was probably the result of it having a lower ROE. We believe that there also might be other aspects that are negatively influencing the company's earnings prospects. Such as - low earnings retention or poor allocation of capital.

However, when we compared Weyerhaeuser's growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 15% in the same period. This is quite worrisome.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. Has the market priced in the future outlook for WY? You can find out in our latest intrinsic value infographic research report.

Is Weyerhaeuser Using Its Retained Earnings Effectively?

Weyerhaeuser seems to be paying out most of its income as dividends judging by its three-year median payout ratio of 63% (meaning, the company retains only 37% of profits). However, this is typical for REITs as they are often required by law to distribute most of their earnings. So this probably explains the company's shrinking earnings.

Moreover, Weyerhaeuser has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 220% over the next three years.

Summary

In total, we would have a hard think before deciding on any investment action concerning Weyerhaeuser. As a result of its low ROE and lack of mich reinvestment into the business, the company has seen a disappointing earnings growth rate. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.