What's in the Cards for Iron Mountain (IRM) in Q2 Earnings?

Iron Mountain Incorporated IRM is slated to release second-quarter 2023 results on Aug 3, before the opening bell. While revenues are expected to have grown year over year, funds from operations (FFO) per share are likely to have been on par with the prior-year quarter’s reported figure.

In the last reported quarter, this real estate investment trust (REIT) delivered a surprise of 4.30% in terms of adjusted FFO (AFFO) per share. Its results reflected solid performance in the storage and service segments, and the data-center business. However, higher operating expenses in the quarter acted as a dampener.

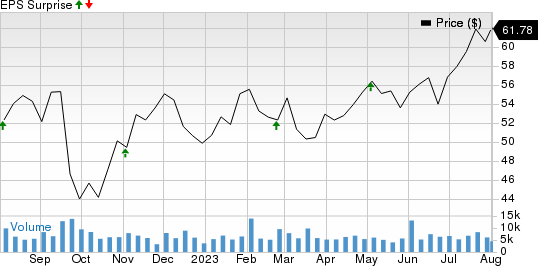

Over the trailing four quarters, Iron Mountain’s FFO per share surpassed the Zacks Consensus Estimate on all occasions, the average beat being 2.93%. The graph below depicts this surprise history:

Iron Mountain Incorporated Price and EPS Surprise

Iron Mountain Incorporated price-eps-surprise | Iron Mountain Incorporated Quote

Factors to Note

During the second quarter, Iron Mountain is likely to have benefited from its stable and resilient core storage and records management businesses. The continued benefit of pricing and positive volume trends is anticipated to have led to healthy storage rental revenues, which account for the lion’s share of IRM’s revenues.

The demand for the company’s traditional services, which comprise charges for related core service activities and a wide array of complementary products and services, and new and existing digital offerings are likely to have remained healthy, aiding service revenue growth.

Also, IRM’s Global Data Center business is expected to have witnessed healthy leasing activity on the back of robust demand for connectivity, interconnection and colocation space, boosting the top line.

Iron Mountain enjoys a diversified tenant and revenue base across different industries and locations and has maintained consistent customer retention over the years. This is expected to have led to stable revenues during the quarter.

The Zacks Consensus Estimate for storage rental revenues is pegged at $824.0 million, suggesting a 1.7% improvement from the prior quarter’s $810.1 million and 9.4% from the year-ago period’s $753.0 million. Our estimate for quarterly storage rental revenues suggests an increase of 6.1% year over year.

The consensus estimate for service revenues is pegged at $529.9 million, indicating a rise of 5.1% from the prior quarter’s $504.3 million but a decline of 1.1% from the year-ago quarter’s $536.0 million. Our estimate for quarterly service revenues indicates growth of 3.3% year over year.

In the first-quarter 2023 earnings presentation, management projected total revenues to be around $1.35 billion, adjusted EBITDA to be roughly $475 million, AFFO to be nearly $270 million and AFFO per share to be 92 cents for the second quarter.

The consensus estimate for quarterly total revenues is pegged at $1.35 billion, suggesting a year-over-year increase of 4.9%.

Further, IRM is likely to have continued with its asset-base expansion into the fast-growing businesses, especially the data center segment, to supplement its storage segment performance and bolster its external growth during the quarter. Its solid balance sheet position is likely to have supported such activities.

However, given that a major part of the company’s business lies outside the United States, exposure to adverse foreign exchange movements might have impeded its quarterly performance to some extent.

The company’s activities during the to-be-reported quarter were inadequate to garner analysts’ confidence. The Zacks Consensus Estimate for the quarterly FFO per share has been revised 1.1% southward to 93 cents over the past two months.

What Our Quantitative Model Predicts

Our proven model does not conclusively predict an FFO beat for Iron Mountain this time. The right combination of two key ingredients — a positive Earnings ESP and a Zacks Rank #3 (Hold) or higher — increases the odds of a beat. However, that is not the case here.

Earnings ESP: IRM has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: IRM currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Stocks That Warrant a Look

Here are some stocks that are worth considering from the REIT sector, as our model shows that these have the right combination of elements to deliver a surprise this reporting cycle:

Ventas VTR is scheduled to report quarterly numbers on Aug 3. VTR has an Earnings ESP of +1.75% and a Zacks Rank #2 currently.

Ryman Hospitality Properties RHP is slated to report quarterly numbers on Aug 3. RHP has an Earnings ESP of +3.87% and carries a Zacks Rank #1 presently.

Americold Realty Trust COLD is scheduled to report quarterly figures on Aug 3. COLD currently has an Earnings ESP of +1.96% and a Zacks Rank #3.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Iron Mountain Incorporated (IRM) : Free Stock Analysis Report

Ventas, Inc. (VTR) : Free Stock Analysis Report

Ryman Hospitality Properties, Inc. (RHP) : Free Stock Analysis Report

Americold Realty Trust Inc. (COLD) : Free Stock Analysis Report