Why You Should Add Integer Holdings (ITGR) to Your Portfolio

Integer Holdings Corporation ITGR has been gaining from its research and product development activities. The optimism led by a solid third-quarter 2023 performance and its solid foothold in the broader MedTech space are expected to contribute further. However, volatility in energy markets and global climate change-related concerns are a hurdle.

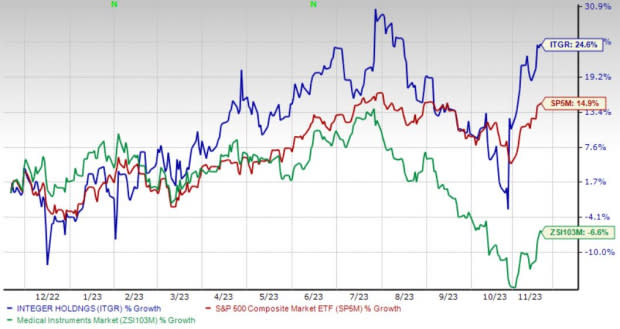

In the past year, this Zacks Rank #1 (Strong Buy) stock has gained 24.6% against a 6.6% decline of the industry. The S&P 500 has witnessed 14.9% growth in the said time frame.

The renowned medical device outsource manufacturer has a market capitalization of $2.97 billion. The company projects 15.8% growth for the next five years and expects to maintain its strong performance. Integer Holdings surpassed the Zacks Consensus Estimate in all the trailing four quarters, delivering an earnings surprise of 11.9%, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strong Q3 Results: Integer Holdings’ robust third-quarter 2023 results raise our optimism. The company registered year-over-year top-line and bottom-line performances. The Medical segment recorded robust results owing to strength in the majority of its product lines. The expansion of both margins bodes well.

Research and Product Development: We are optimistic about Integer Holdings’ position as a developer and manufacturer of medical devices and components. The company is focused on developing new products, improving and enhancing existing products and expanding the use of its products in new or tangential applications. In addition to ITGR’s internal technology and capability development efforts aimed at providing its customers with differentiated solutions, the company engages outside research institutions for unique technology projects.

Solid Foothold in the Broader MedTech Space: We are optimistic about Integer Holdings’ stable footing in the cardiac, neuromodulation, orthopedics, vascular and advanced surgical markets. Its primary customers include large, multi-national original equipment manufacturers and their affiliated subsidiaries.

ITGR is focused on sales efforts to increase its market penetration in the Cardio & Vascular, Neuromodulation and Non-Medical Electrochem markets. The company is undertaking strategic initiatives to maintain its leadership position in the cardiac rhythm management market.

Downsides

Global Climate Change: Customer, investor and employee expectations relating to environmental, social and governance (ESG) have been rapidly evolving and increasing. Also, government organizations are enhancing or advancing legal and regulatory requirements specific to ESG matters. The heightened stakeholder focus on ESG issues related to ITGR’s business requires the continuous monitoring of various and evolving laws, regulations, standards and expectations and the associated reporting requirements. A failure to adequately meet stakeholders’ expectations may result in non-compliance, loss of business and reduced demand for Integer Holdings’ stock, among others.

Volatility in Energy Markets: Sales of Integer Holdings’ products into the energy market depends upon the condition of the oil and gas industry. Currently, oil and natural gas prices have been subject to significant fluctuation. Per management, a change in the oil and gas exploration and production industry or a reduction in the exploration and production expenditures of oil and gas companies could cause the company’s energy market revenues to decline.

Estimate Trend

Integer Holdings is witnessing a positive estimate revision trend for 2023. In the past 90 days, the Zacks Consensus Estimate for earnings has moved 6% north to $4.59 per share.

The Zacks Consensus Estimate for the company’s fourth-quarter 2023 revenues is pegged at $396.5 million, suggesting a 6.5% rise from the year-ago quarter’s reported number.

Other Key Picks

A few other top-ranked stocks in the broader medical space are DaVita Inc. DVA, HealthEquity, Inc. HQY and Cardinal Health, Inc. CAH.

DaVita, sporting a Zacks Rank #1 at present, has an estimated long-term growth rate of 18.3%. DVA’s earnings surpassed estimates in all the trailing four quarters, with an average surprise of 36.6%. You can see the complete list of today’s Zacks #1 Rank stocks here.

DaVita has gained 35.3% compared with the industry’s 4.7% rise over the past year.

HealthEquity, flaunting a Zacks Rank of 1 at present, has an estimated long-term growth rate of 26.7%. HQY’s earnings surpassed estimates in all the trailing four quarters, with an average of 13%.

HealthEquity has gained 6.9% against the industry’s 12.4% decline over the past year.

Cardinal Health, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 15.2%. CAH’s earnings surpassed estimates in all the trailing four quarters, with an average surprise of 15.7%.

Cardinal Health has gained 33% compared with the industry’s 10.4% rise over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DaVita Inc. (DVA) : Free Stock Analysis Report

Cardinal Health, Inc. (CAH) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report

Integer Holdings Corporation (ITGR) : Free Stock Analysis Report