Why American Woodmark Corporation’s (NASDAQ:AMWD) High P/E Ratio Isn’t Necessarily A Bad Thing

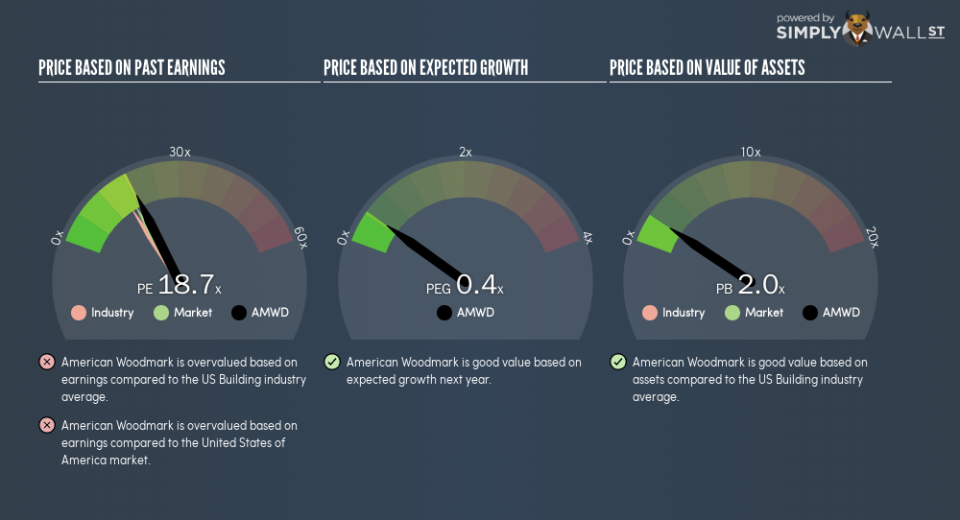

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). To keep it practical, we’ll show how American Woodmark Corporation’s (NASDAQ:AMWD) P/E ratio could help you assess the value on offer. American Woodmark has a price to earnings ratio of 18.73, based on the last twelve months. In other words, at today’s prices, investors are paying $18.73 for every $1 in prior year profit.

Check out our latest analysis for American Woodmark

Want to help shape the future of investing tools and platforms? Take the survey and be part of one of the most advanced studies of stock market investors to date.

How Do You Calculate A P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for American Woodmark:

P/E of 18.73 = $69.75 ÷ $3.72 (Based on the trailing twelve months to October 2018.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that buyers have to pay a higher price for each $1 the company has earned over the last year. That isn’t a good or a bad thing on its own, but a high P/E means that buyers have a higher opinion of the business’s prospects, relative to stocks with a lower P/E.

How Growth Rates Impact P/E Ratios

P/E ratios primarily reflect market expectations around earnings growth rates. Earnings growth means that in the future the ‘E’ will be higher. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. A lower P/E should indicate the stock is cheap relative to others — and that may attract buyers.

American Woodmark saw earnings per share decrease by 18% last year. But over the longer term (5 years) earnings per share have increased by 22%.

How Does American Woodmark’s P/E Ratio Compare To Its Peers?

The P/E ratio essentially measures market expectations of a company. You can see in the image below that the average P/E (15.8) for companies in the building industry is lower than American Woodmark’s P/E.

Its relatively high P/E ratio indicates that American Woodmark shareholders think it will perform better than other companies in its industry classification. Clearly the market expects growth, but it isn’t guaranteed. So investors should always consider the P/E ratio alongside other factors, such as whether company directors have been buying shares.

Don’t Forget: The P/E Does Not Account For Debt or Bank Deposits

The ‘Price’ in P/E reflects the market capitalization of the company. In other words, it does not consider any debt or cash that the company may have on the balance sheet. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

American Woodmark’s Balance Sheet

Net debt totals 55% of American Woodmark’s market cap. If you want to compare its P/E ratio to other companies, you should absolutely keep in mind it has significant borrowings.

The Verdict On American Woodmark’s P/E Ratio

American Woodmark’s P/E is 18.7 which is above average (17.1) in the US market. With significant debt and no EPS growth last year, shareholders are betting on an improvement in earnings from the company.

Investors have an opportunity when market expectations about a stock are wrong. People often underestimate remarkable growth — so investors can make money when fast growth is not fully appreciated. So this free report on the analyst consensus forecasts could help you make a master move on this stock.

But note: American Woodmark may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.