Taxes.

Everyone has to pay them and almost nobody likes doing it. Especially US corporations.

But in the wake of Donald Trump’s victory in Tuesday’s election, it seems likely that changes are coming to America’s tax system.

And this is great news for corporate earnings.

During his campaign, Trump outlined plans to lower the US corporate tax rate to 15%. In a note to clients published Thursday, analysts at Goldman Sachs (GS) outlined how a reduction in the top-line tax rate paid by corporates could impact their bottom lines.

In short, it would be huuuge.

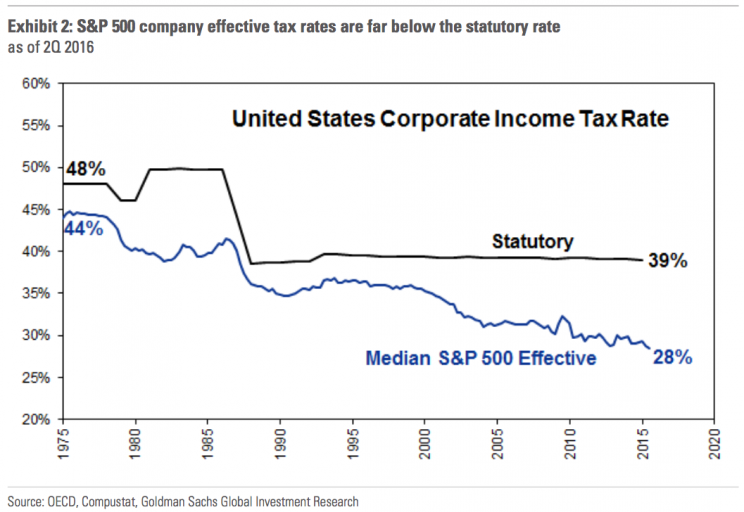

Right now, the statutory tax rate paid by S&P 500 (^GSPC) companies is 39%. Almost no company pays this rate. The effective tax rate, or what companies actually pay, is around 28%.

And as Goldman notes, every 1% decline in the effective tax paid by companies adds $1.50 to the S&P 500’s collective earnings per share. This is significant considering S&P earnings per share are just over $100.

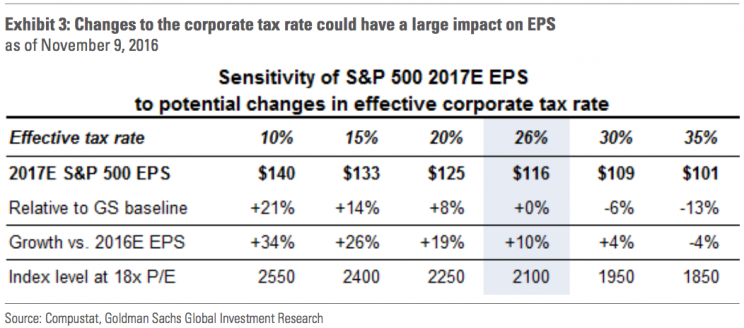

In its note, Goldman assumes a Trump tax cut could pass in 2017 but that the actual statutory rate would be closer to the 28% effective rate currently paid by the S&P 500 rather than the 15% proposed by Trump. But a 28% (or so) statutory rate would yield an effective rate somewhere between 15%-20%. And this could see 2017 earnings rise by around 20% against 2016. Which would be good for stocks.

Keeping the valuation of the S&P 500 steady at 18 times earnings, the level of the benchmark index could rise to 2,250 or even 2,400 depending on where tax rates settled.

This would be a roughly 5%-15% rise in the level of the S&P 500.

A tax cut could also compound the already-positive news we’re starting to see out of corporate earnings, which appear set to rise for the first time in over a year.

In late October, S&P 500 earnings growth turned positive, with blended earnings rising 1.6% over the prior year, for the first time since the first quarter of 2015. As of last Friday, blended earnings were up 2.7%, according to data from FactSet.

And so corporate America’s so-called “earnings recession” — which was impacted by the crash in oil prices and the rise in the US dollar — looks set to end just as US corporates get another boost from a potential tax cut.

Cash coming back to America

Trump also outlined in his tax plan a proposal for a one-time tax holiday for US companies to repatriate cash held abroad, or bring money parked overseas back to the US.

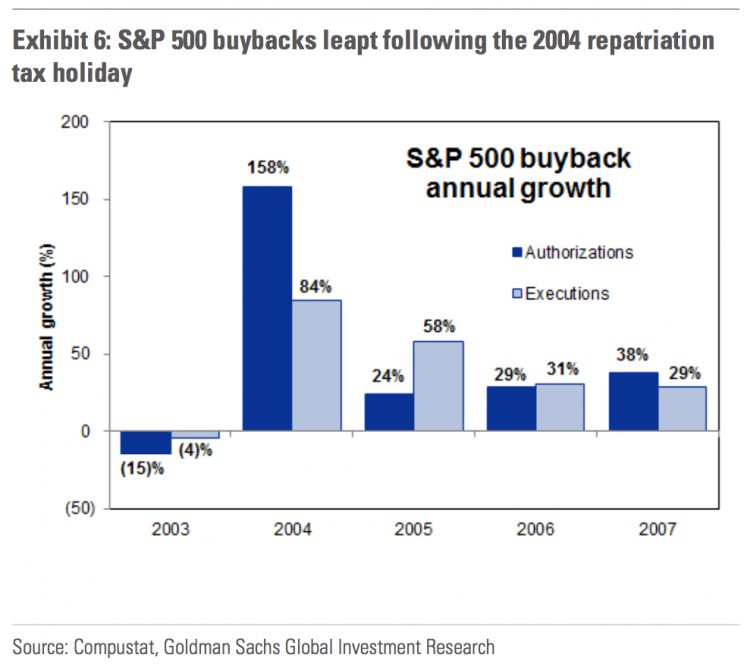

Goldman previously explored this issue and found that this “tax holiday” would likely flop, given that the motivation behind it is to get cash back in the US investing in the US. Not, as previous experiences have seen, resulting in stock buybacks.

“The 2004 precedent suggests a large amount of repatriated cash would be used for buybacks, which would boost stock performance and per-share earnings,” Goldman writes.

“Following the passage of a similar tax holiday in 2004, US companies repatriated $300 billion in cash. S&P 500 buybacks rose by 84% in 2004 and 58% in 2005.”

This is good for shareholders, but not necessarily good for the average worker.

Or as Yahoo Finance’s Rick Newman wrote Wednesday, elites are already benefitting from President Trump.

Two risks

Stocks are taking a breather on Friday in a slow day of trading — bond markets are closed for Veteran’s Day — but for the two days following Trump’s election, stocks were in rally mode with the Dow hitting a record high on Thursday.

But there are still some hurdles for markets to overcome in order for these shareholder-friendly scenarios to play out.

For starters, the whole tax cut thing might not go to plan.

“Despite investor enthusiasm, substantial uncertainty remains regarding the likelihood, timing, and details of potential tax reform,” Goldman writes.

“President-elect Trump will not take office for another two months, and then the process of negotiation, drafting, and voting will begin. Given the implications of potential tax reform on government revenue and the deficit, it is likely that some in Congress will oppose the magnitude of tax cuts proposed during Trump’s candidacy.”

Additionally, bond yields have risen sharply following Trump’s election, which while hurting existing bond investors could make fixed income more attractive relative to stocks after years of falling or record-low rates.

“In addition, the impact on equity prices from lower taxes and higher earnings may be offset by lower valuations if rates continue to rise,” Goldman writes.

“During the last few days, US 10-year Treasury yields have risen by roughly 30 bp as the market priced expectations of faster growth and inflation. Historically low rates lifted US equity valuations to near-record highs, and if risk-free rates continue to rise they may result in lower equity valuations.”

—

Myles Udland is a writer at Yahoo Finance.

Read more from Myles here; follow him on Twitter @MylesUdland