Why a Hold Strategy is Apt for ExlService (EXLS) Stock Now

ExlService Holdings, Inc. EXLS is an excellent strategic partner for data-led businesses and has a large addressable market.

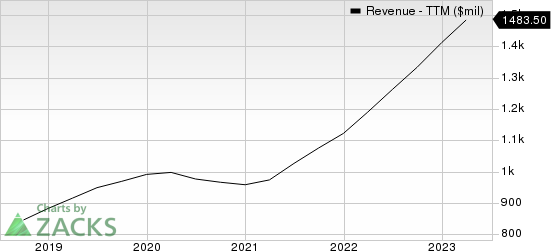

The company’s earnings for 2023 and 2024 are expected to increase 14.3% and 14.1%, respectively. Revenues are expected to grow 14.5% and 12.4%, respectively, in 2023 and 2024.

Tailwinds

ExlService is an excellent strategic partner for data-led businesses. The company’s market differentiation strategy hovers around applying the combination of data-led capabilities and domain expertise. Advanced analytics, data and AI-based digital solutions are helping the company develop and bring integrated services and solutions under one brand.

EXLS has a large addressable market that includes healthcare, banking, insurance, retail, media and technology industries. It remains focused on expanding its presence in both well-established and emerging markets, building its client portfolio in finance and accounting and consulting services across all its business segments.

ExlService Holdings, Inc. Revenue (TTM)

ExlService Holdings, Inc. revenue-ttm | ExlService Holdings, Inc. Quote

ExlService has a consistent record of share repurchases. It repurchased shares worth $68.5 million, $115.6 million and $77.8 million in 2022, 2021 and 2020, respectively. Such moves help instill investors’ confidence in the stock and positively impact earnings per share.

Some Risk

EXLS’ current ratio (a measure of liquidity) at the end of the first quarter of 2023 was 2.02, lower than the prior quarter’s current ratio of 2.21 and the year-ago quarter’s 2.58. A decline in the current ratio is not desirable as it indicates that the company may have problems meeting its short-term debt obligations.

Zacks Rank and Stocks to Consider

ExlService currently carries a Zacks Rank #3 (Hold). Investors interested in the broader Zacks Business Services industry can consider the following better-ranked stocks:

Green Dot GDOT: For second-quarter 2023, the Zacks Consensus Estimate for Green Dot’s revenues suggests a decline of 4.8% year over year to $338.2 million and the same for earnings indicates a 59.5% plunge to 30 cents per share. The company has an impressive earnings surprise history, beating the consensus mark in all the trailing four quarters, the average surprise being 37.3%.

GDOT has a Value Score of A and a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Maximus MMS: For second-quarter 2023, the Zacks Consensus Estimate for Maximus’ revenues suggests an increase of 6.9% year over year to $1.2 billion and the same for earnings indicates a 46.2% rise to $1.14 per share. The company has an impressive earnings surprise history, beating the consensus mark in three instances and missing once, the average surprise being 9.6%.

MMS has a VGM Score of B and a Zacks Rank of 1.

Rollins ROL: For second-quarter 2023, the Zacks Consensus Estimate for Rollins’ revenues suggests growth of 12.6% year over year to $803.6 million and the same for earnings indicates a 15% increase to 23 cents per share. The company has an impressive earnings surprise history, beating the consensus mark in three of the trailing four quarters and missing once, the average surprise being 5.53%.

ROL currently carries a Zacks Rank of 2 and a Growth Score of A.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Green Dot Corporation (GDOT) : Free Stock Analysis Report

ExlService Holdings, Inc. (EXLS) : Free Stock Analysis Report

Rollins, Inc. (ROL) : Free Stock Analysis Report

Maximus, Inc. (MMS) : Free Stock Analysis Report