Why Prudent Investors Are Snapping Up Ensign (ENSG) Stock Now

The Ensign Group, Inc. ENSG is well-poised to grow due to the rising demand for skilled post-acute services and growth in occupancy. Its solid and disciplined inorganic growth strategy also continues to aid its performance.

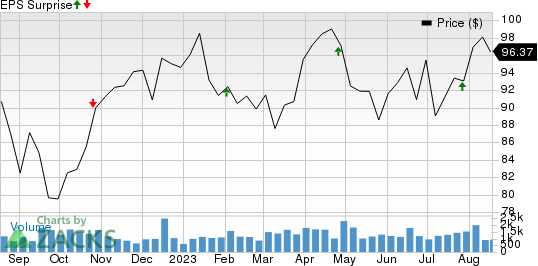

Outperformance & Zacks Rank

Over the past three months, shares of Ensign have risen 4.9%, outperforming the industry’s 7.7% decline. Headquartered in San Juan Capistrano, CA, ENSG operates as a provider of skilled nursing, senior living, rehabilitative and other services. With a market cap of $5.5 billion, it also has a profitable real estate business operation.

Due to its solid prospects, this Zacks Rank #2 (Buy) stock is worth adding to your portfolio at the moment.

Let’s delve deeper.

The Zacks Consensus Estimate for Ensign’s current-year earnings is pegged at $4.71 per share, which has witnessed one upward estimate revision in the past 30 days against none in the opposite direction. The estimate indicates 13.8% year-over-year growth. Ensign beat on earnings in two of the last four quarters, met once and missed the same on the other occasion, the average surprise being 0.9%.

The Ensign Group, Inc. Price and EPS Surprise

The Ensign Group, Inc. price-eps-surprise | The Ensign Group, Inc. Quote

The consensus mark for current-year revenues is pegged at $3.7 billion. Rising service and rental revenues are likely to support its top-line growth. Our estimate for service revenues for 2023 suggests more than 22% year-over-year growth.

Our estimate suggests total Medicaid and Medicare revenue growth for 2023 of nearly 21%. A strong skilled mix and occupancy growth will continue boosting its results. We expect occupancy levels to rise to 78.6% in 2023 from the 2022 level of 75.3%.

ENSG’s acquisition pipeline remained steady during the summer, and management expects to witness more opportunities in the fall. At the start of this month, its portfolio grew to 293 healthcare operations due to strategic buyouts, of which 26 incorporated senior living operations. Its growing footprint in a diversified market is likely to allow it to capture a better market share.

The company now owns 112 real estate assets. Its balance sheet strength is likely to continue supporting its acquisition efforts. Its long-term debt to capital of 9.6% compares favorably with the industry’s average of 74.6%.

A Risk

However, there is a factor that investors should keep a careful eye on.

Ensign’s persistent increase in total expenses is affecting its margins. Our estimate for 2023 expenses suggests a 23.8% year-over-year increase. Nevertheless, we believe that a systematic and strategic plan of action will drive growth in the long term.

Other Key Picks

Some other top-ranked stocks in the medical space are HCA Healthcare, Inc. HCA, Atai Life Sciences N.V. ATAI and Select Medical Holdings Corporation SEM, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for HCA Healthcare’s 2023 bottom line suggests a 9.1% increase from the prior-year levels. HCA has witnessed seven upward estimate revisions in the past 30 days against none in the opposite direction. It beat earnings estimates in three of the last four quarters and missed once, with the average surprise being 5.4%.

The Zacks Consensus Estimate for Atai Life Sciences’ current-year earnings indicates a 16.3% improvement from the year-ago reported figure. It has witnessed four upward estimate revisions over the past week against no movement in the opposite direction. ATAI beat earnings estimates in two of the last four quarters, met once and missed the same on the other occasion.

The Zacks Consensus Estimate for Select Medical’s 2023 earnings indicates a 56.9% year-over-year increase to $1.93 per share. It has witnessed one upward estimate revision over the past month against no movement in the opposite direction. The consensus mark for SEM’s 2023 revenues predicts 4.2% growth from a year ago.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

HCA Healthcare, Inc. (HCA) : Free Stock Analysis Report

Select Medical Holdings Corporation (SEM) : Free Stock Analysis Report

atai Life Sciences N.V. (ATAI) : Free Stock Analysis Report

The Ensign Group, Inc. (ENSG) : Free Stock Analysis Report