Why Snap (NYSE:SNAP) Could Become a Penny Stock

Snap (NYSE:SNAP) may be heading toward penny stock status. Back in December, I urged investors to consider exiting their positions at $15.90 due to an unjustified surge in the stock. Fast-forward to today, with Snap trading at $11.31, and my bearish outlook on Snap has only deepened. Following continuous operating losses and a lack of substantial free cash flow generation to justify its current valuation, Snap seems poised to keep deteriorating shareholder value, inevitably inching closer to penny stock status.

Snap’s Growth Stalls as Peers Surge

The first factor fueling my bearish stance on Snap is its stagnant growth in a landscape where its peers thrive and deliver great results. Assuming Snap was growing rapidly, I could go easier on the company’s disastrous profitability (more on that later). However, with top-line growth having halted, I see no way for the company to come out of its current predicament.

To illustrate, Snap’s revenues came in at $4.6 billion in FY 2023, flat compared to the previous year. This result is quite underwhelming in itself because Snap’s revenue growth stagnated during a rather favorable advertising environment. In fact, many of its peers in the social media and content-sharing area recorded significantly higher revenues during the same period.

For instance, Meta Platforms (NASDAQ:META) posted revenue growth of 16% last year, while Alphabet’s (NASDAQ:GOOGL)(NASDAQ:GOOG) YouTube also grew its revenues by 16% in this period. Even Pinterest, whose growth tends to underperform, grew its top line by 9% in FY 2023.

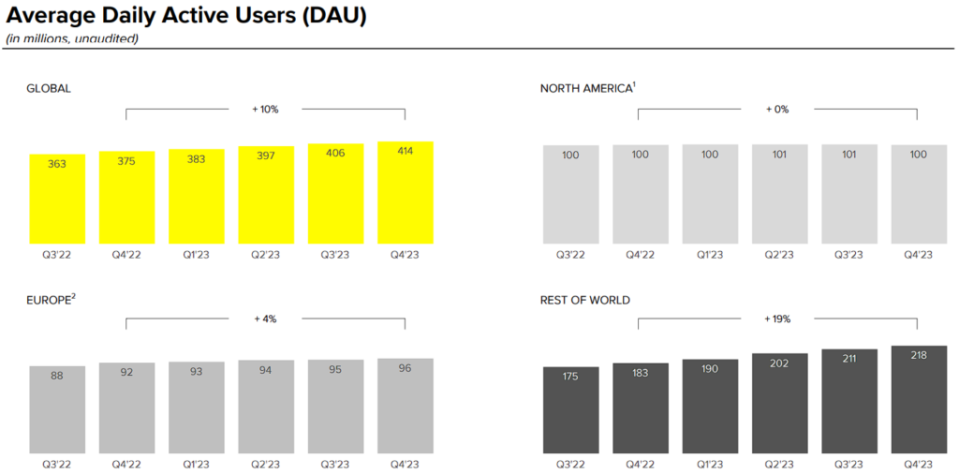

The company may highlight its platform’s ongoing user growth, with Snap’s daily active users rising to 414 million globally in Q4—marking a 10% increase. However, this narrative merely scratches the surface. Notably, this expansion is primarily attributed to a 19% surge in users from the rest-of-the-world regions (i.e., all regions outside North America and Europe).

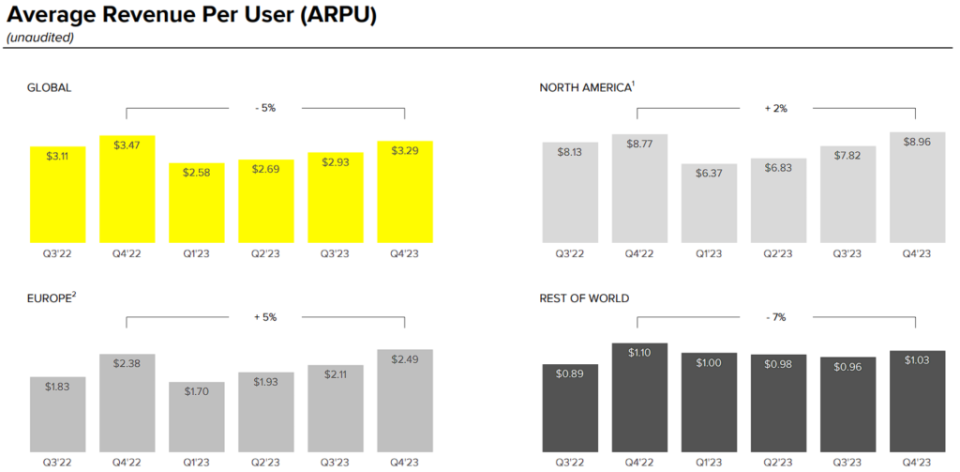

The problem is that RoW user growth has little to no value, as these users can hardly be monetized. It is actually North America and Europe that can drive ad revenue, as their users have tremendously higher purchasing power. In the meantime, Snap even lost about one million users quarter-over-quarter in North America, further dampening its user mix. Therefore, despite the seemingly growing user base, Snap’s revenue per user (ARPU) fell by 5% in Q4, partially offsetting revenue gains from user growth.

Snap’s quarterly reports have consistently highlighted advertisers’ hesitation to spend big on its platform relative to its competitors, likely largely due to the lack of impactful conversion metrics. Thus, given that Snap posted a decline in ARPU in a vigorous advertising environment, it’s reasonable to expect that the moment global ad spending loses its current steam in line with its cyclical fashion, Snap’s revenues could plummet from here.

Operating Losses Persist & Free Cash Flow Isn’t a Good Indicator

With Snap lacking meaningful revenue growth to improve its profitability prospects, its operating losses are likely to persist. At the same, the company’s seemingly growing free cash flow model isn’t a good indicator of the stock’s prospects, as Snap’s stock-based compensation (SBC) keeps deteriorating shareholder value. Let’s take a deeper look.

As you can see below, with total costs and expenses surpassing Snap’s revenues, FY 2023 marked another year of steep operating losses, reaching $1.4 billion.

Snap may defend its position in that regard by citing its “growing” free cash flow. In fact, management celebrated FY 2023 as Snap’s third consecutive year of positive free cash flow. However, Snap’s free cash flow should be highly scrutinized. Take a look at Snap’s FY 2023 statements. You will find that while free cash flow came in came in at roughly $35 million, this number includes a huge $1.3 billion in stock-based compensation expenses added back during the reconciliation process.

Therefore, while it may seem that Snap “creates value” due to its positive free cash flow, the rate at which it dilutes shareholders (with FY 2023’s SBC equal to about 7% of the current market cap) more than offsets the rate at which value is created by a wide margin.

In my view, this trend appears poised to persist, steadily chipping away at shareholders’ equity per share, resulting in increasing dilution and, thus, a declining share price. This trajectory will potentially drive Snap toward penny stock territory. With no apparent catalysts for revenue growth and a persistent struggle to control expenses, the course seems irreversible.

This process could even accelerate if ARPU keeps falling, which I find increasingly likely, given the company’s lackluster performance during a favorable ad environment.

Is SNAP Stock a Buy, According to Analysts?

Wall Street seems to have mixed feelings about the stock, as SNAP features a Hold consensus rating based on nine Buys, 22 Holds, and two Sell ratings assigned in the past three months. At $13.98 per share, the average SNAP stock price target suggests 23.6% upside potential.

If you’re wondering which analyst you should follow if you want to buy and sell SNAP stock, the most accurate analyst following the stock (on a one-year timeframe) is Ross Sandler from Barclays. He boasts an average return of 43.94% per rating and a 57% success rate.

The Takeaway

In conclusion, I understand that suggesting Snap is headed towards penny stock territory may appear audacious. Nonetheless, from my perspective, it seems increasingly inevitable.

Despite management’s attempts to highlight growing user numbers and positive free cash flow, the company faces significant hurdles. Stalled revenue growth, troubled by a decline in ARPU and persistent operating losses, paints a bleak picture.

With competitors surging and advertisers hesitant to spend their hard-earned dollars on Snap’s platform, it’s only reasonable to expect the company’s metrics to worsen further, particularly once global ad spending takes a breather, which could accelerate the erosion in shareholder value.