Why Should You Stay Invested in Horace Mann (HMN) Stock Now?

Horace Mann Educators Corporation’s HMN strategic initiatives to fuel profitability, its niche market focus, a solid capital position and favorable growth estimates make it a good investment choice.

Horace Mann has a favorable VGM Score of B. This helps to identify stocks with the most attractive value, growth and momentum.

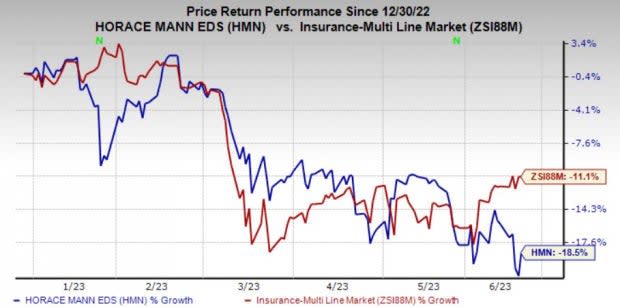

Zacks Rank & Price Performance

Horace Mann currently carries a Zacks Rank #2 (Buy). Year to date, the stock has declined 18.5% versus the industry’s increase of 11.1%.

Image Source: Zacks Investment Research

Optimistic Growth Projection

The Zacks Consensus Estimate for 2023 earnings is pegged at $1.88, indicating an increase of 24.5% on 8% higher revenues of $1.5 billion. The consensus estimate for 2024 earnings is pegged at $3.23, indicating an increase of 71.8% on 5.3% higher revenues of $1.6 billion.

Earnings Surprise History

The insurer has a solid record of delivering an earnings surprise in the last four quarters, with the average beat being 41.65%.

Business Tailwinds

Horace Mann, the largest financial services company serving the U.S. educator market, is well-poised to capitalize on the solid opportunity in the K-12 educator market. A 4% increase in K-12 teachers is anticipated between 2023 and 2028.

Further, a demographic shift is expected as baby boomers retire and millennials make up a higher percentage of the workforce. HMN, banking on a compelling portfolio, is well-placed to capitalize on the opportunity, given its strategic focus on designing products. The addition of Supplemental products has enhanced cross-selling.

In fact, in 2023, the insurer aims net premiums and contract charges earned to be primarily driven by Supplemental & Group Benefits. Also, banking on solid first-quarter performance, the company estimates Supplemental & Group Benefits segment core earnings between $45 million and $49 million in 2023.

Horace Mann remains focused on improving product offerings, strengthening distribution and modernizing infrastructure. The insurer expects to continue to improve pricing.

The company intends to increase auto rates by 18% to 20% by 2023. In property, HMN expects to increase rates by 12% to 15% through 2023. It expects rate increases and non-rate actions to contribute to nationwide premium increases of 17% to 20%.

Horace Mann targets a combined ratio between 95 and 96 over the longer term and auto combined ratio between 97% and 98% in 2024.

The company estimates generating about $50 million in excess capital annually to support growth initiatives, buy back shares and hike dividends.

HMN targets core earnings per share between $2 and $2.30 in 2023, near $4 in 2024 and 10% average annual EPS growth over the long term.

Horace Mann looks to deliver a double-digit return on equity over the long term.

Impressive Dividend History

Banking on operational excellence, Horace Mann increased its dividend for 15 straight years at a CAGR of 14%. Its current dividend yield of 4.3% is higher than the industry average of 2.8%. HMN targets a 50% dividend payout over the medium term.

Stocks to Consider

Some better-ranked stocks from the property and casualty insurance industry are Kinsale Capital Group, Inc. KNSL, RLI Corp. RLI and Root, Inc. ROOT. While RLI Corp. sports a Zacks Rank #1 (Strong Buy), Kinsale Capital and Root carry a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Kinsale Capital has a solid track record of beating earnings estimates in each of the last trailing four quarters, the average being 14.77%. In the past year, KNSL has gained 71.7%.

The Zacks Consensus Estimate for KNSL’s 2023 and 2024 earnings per share is pegged at $10.37 and $12.41, indicating a year-over-year increase of 32.9% and 19.6%, respectively.

RLI beat estimates in each of the last four quarters, the average being 43.50%. In the past year, RLI has gained 20.6%.

The Zacks Consensus Estimate for RLI’s 2023 and 2024 earnings has moved 10.1% and 3.7% north, respectively, in the past 60 days.

Root beat estimates in each of the last four quarters, the average being 18.24%. In the past year, the insurer has lost 71.9%.

The Zacks Consensus Estimate for ROOT’s 2023 and 2024 earnings per share indicates a year-over-year increase of 43.8% and 42.5%, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

RLI Corp. (RLI) : Free Stock Analysis Report

Horace Mann Educators Corporation (HMN) : Free Stock Analysis Report

Kinsale Capital Group, Inc. (KNSL) : Free Stock Analysis Report

Root, Inc. (ROOT) : Free Stock Analysis Report