William Blair Commentary: Clouds Clearing in the Land of the Rising Sun

On the back of five recent trips to Japan, our global equity team has been increasing Japanese equity exposure across our international strategies over the past few quarters, narrowing the underweights we had for some time.

There are three reasons, but before I delve into them, let me explain why we were underweight Japan in the first place.

Decades of Stagnation

From the 1970s through the 1990s, Japan was a world leader. Its economy was growing, and it was a dominant player in a few different industries. Then its nominal gross domestic product (GDP) growth began to stagnate due to a complex interplay of factors.

The bursting of the asset-price bubble in the late 1980s led to a severe economic downturn, exposing weaknesses in the banking sector and constraining credit availability.

Additionally, Japan's aging population, characterized by a declining birth rate and increasing life expectancy, resulted in a shrinking workforce and deflationary pressures. Deflation puts an economy in neutral as individuals and businesses delay spending in anticipation of lower prices in the future.

Other factors influencing Japan's stagnation included structural challenges such as rigid labor markets, inefficient corporate governance practices, and limited immigration, which further hindered innovation and productivity gains.

Moreover, Japan's high public debt levels constrained fiscal policy flexibility, limiting the government's ability to implement aggressive stimulus measures.

Breaking Japan's GDP into two componentscorporate profits and wageswe observe that over the past 30 years, nominal wages have been negative or flat. In that environment, corporate profits won't grow because consumer spending drives a significant portion of economic activity and corporate revenue. When nominal wages are stagnant or declining, consumers have less disposable income to spend on goods and services. This, in turn, affects equity prices.

In this environment, businesses deleveraged. From the mid-1990s until about 2010, when Abenomics (the economic policies advocated by former Prime Minister Shinzo Abe) came into play, corporations were paying down debt, and it's hard for an economy to grow when debt isn't being used to fund investments and drive growth.

These phenomena all combined to weigh on economic activity, and in that type of environment, we weren't finding quality growth opportunities. We look at characteristics such as return on invested capital, revenue growth, operating margin, free cash flow margin, and return on equityand in all of these, Japan has trailed the United States, Europe, the United Kingdom, China, and most of our investable universe. So, we were simply finding better opportunities elsewhere.

But we're now more bullish on Japan. I highlight three specific reasons below.

An Improving Macro Environmentfor the First Time in Decades

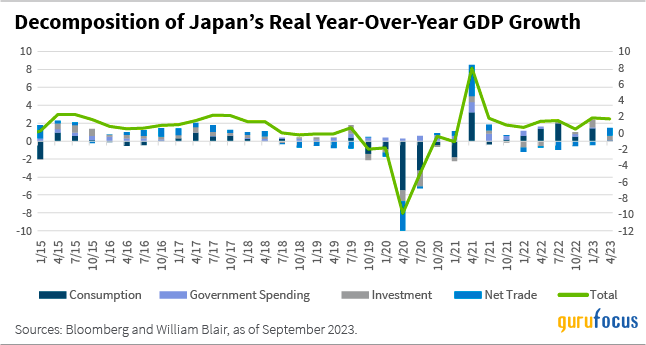

First, we believe the macro environment is becoming more conducive for investors. If we look at the decomposition of Japan's real GDP growth year over year, we can see that it's starting to come from consumption.

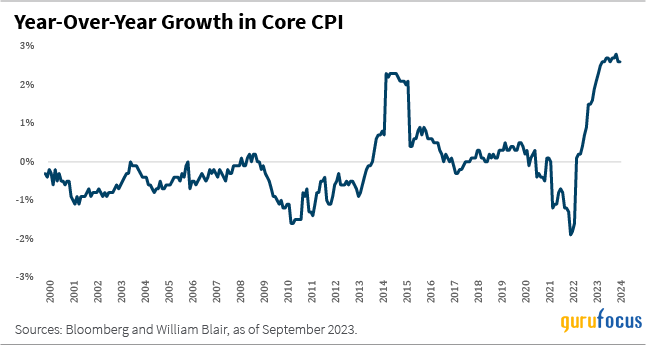

That means people are actually spending money. And after decades of zero inflation or deflation, Japan is finally experiencing inflation.

The question is, are the growth in GDP and uptick in inflation sustainable? We believe so, because Japan's labor market has changed, making wage gains more likely, and that would be an indication that the inflation and consumption story are sustainable, which is potentially good for the economy and good for the stock market.

One of Abenomics' three arrows, which sought to revive the stagnant Japanese economy, involved structural reforms to increase labor force participationin particular, to get more women into the workforce. This push was successful, with Japan becoming a world leader in so-called womenomics. According to Gavecal Research/Macrobond, labor force participation for women aged 15 to 64 is 74% for Japan vs. 66% for the Organisation for Economic Co-operation and Development (OECD) more broadly (and 65% for the United States).

Even with labor force participation increasing over the past decade, there are now roughly two job openings for every job seeker in Japan. The unemployment rate is 2.4%, down from 5% 15 years ago. That illustrates how tight Japan's labor market isand a tight labor market typically leads to wage growth. Indeed, positive nominal wage growth is starting to come through in the data (although it's negative in real terms because inflation is relatively high).

This is similar to what we saw in the United States and Europe a couple of years ago: Real wage changes were initially negative as inflation increases outpaced wages. But then, as broader inflation normalized, those economies experienced positive real wage growth. That's a very good thing for an economy, and it's what we expect to happen in Japan.

Structural Tailwinds Developing

A second reason we're increasing exposure to Japan is that we've seen several reforms that could act as structural tailwinds.

Corporate Governance Reforms

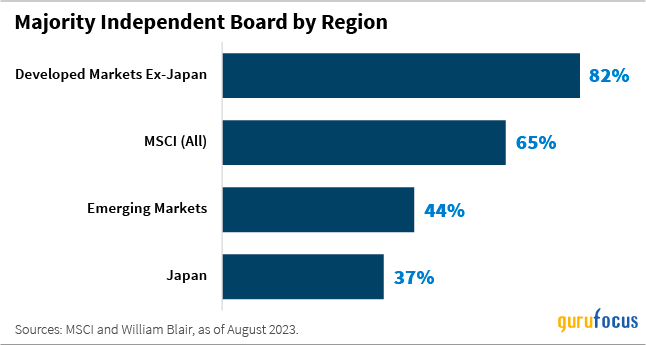

In terms of board independence, separation of CEO and chair, and female directors, Japanese companies rank well behind its developed market peers and even behind most emerging markets. Japanese companies also have the highest number of directors over age 70 (which isn't surprising, given its demographics).

Recent revisions to Japan's corporate governance code, effective April 2022, seek to tackle all of this. For example, they seek to have a minimum of one-third of board directors independent and more women on boards (setting a target of one female director by 2025 and 30% female directors by 2030). Other factors include timely disclosures in English and the availability of an electronic voting platform.

These corporate governance improvements should create better alignment between decision-makers and investors, which we believe will lead to enhanced risk management, better decision-making that focuses on value creation, and ultimately, better shareholder return.

Stock Exchange Reforms

Many Japanese companies desperately need to improve returns and capital efficiency.

For example, 43% of Japanese stocks listed on the TOPIX 500 have a price-to-book (P/B) ratio less than one, meaning you can buy the company for less than its book value. In the United States (S&P 500 Index), that number is just 5%, and in Europe (STOXX 600 Index) 24%.

Similarly, 40% of Japanese stocks listed on the TOPIX 500 have a return on equity of less than 8%. In the United States, that number is just 14%, and in Europe 19%.

The Tokyo Stock Exchange is leading reforms by urging all companies with a P/B ratio of less than one or return on equity of less than 8% to devise a plan to improve capital efficiency and promote investment. Companies that do not develop such a plan will be named and could be delisted.

We believe this name-and-shame campaign should lead to good outcomes for the companies and its investors. Companies may exit or sell off unprofitable businesses, mergers and acquisitions activity may increase, companies may buy back shares and reduce cross-shareholdings in other corporations, and management buyouts may increase. And as we start to see consolidation, the remaining public companies should become more efficient and investor friendly.

Tax Incentive Reforms

A third structural tailwind is a change to Nippon Investment Savings Accounts (NISAs) designed to drive domestic flows into equities.

NISAs are tax-exempt investment accounts designed to encourage personal investment in stocks and mutual funds by offering tax exemptions on capital gains and dividends from investments held within these accounts.

New NISA rules that take effect in January 2024 increase annual and lifetime limits and make the tax incentive timeline (previously five years) unlimited. This, Japan hopes, will turn the trillions of yen held in cash by households into equity investments.

The new NISA rules, when combined with an uptick in inflation, create a significant incentive to put cash into financial instruments rather than a savings accountwhich we believe will drive flows into domestic equities, where Japanese retail investors aren't investing in their own equity market. This could be a multiyear liquidity event for Japanese financial instruments.

A Compelling Bottom-up Story

Lastly, groups of global equity team members have traveled to Japan five times since the fall of 2022, meeting with more than 300 companies, and all returned with a positive outlooknot just because of the macro outlook, but because of the potential for multiples to expand.

The companies we spoke to believe disinflation is dead, inflation is real, and they can finally pass on price increases to the consumer. That has not been culturally acceptable in Japan for a long time as inflation has been near zero. The companies we spoke to also confirmed plans to increase wages as prices are passed through. Many also referenced the focus of the exchanges and investors on increasing returns, profitability, and efficiency.

So, what we are seeing is bottom-up confirmation of a compelling top-down story. At the same time, we can learn more about how individual companies plan to execute through this new environment. We will continue to focus on high-quality companies with strong pricing power and where we believe profitability and total shareholder return are likely to improve.

Thus, we believe Japan presents compelling investment opportunities, and we've been increasing exposure to Japanese equities across our international equity portfolios over the past several months.

Kyle Concannon, CFA, CAIA, is a portfolio specialist for William Blair's global equity strategies.

This article first appeared on GuruFocus.