Woodward (WWD) Gains 34.5% YTD: Will the Uptrend Continue?

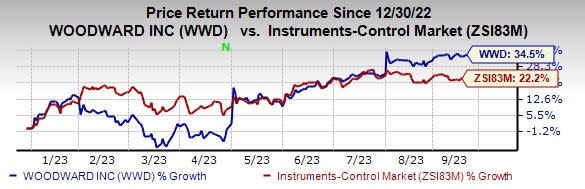

Woodward WWD witnessed strong momentum year to date, with its shares up 34.5% in the same time frame compared with the sub-industry’s growth of 22.2%.

The company is a leading designer, manufacturer and service provider of energy control and optimization solutions. The company provides a wide array of products for fuel, combustion, fluid, actuation and electronic applications, which serve the commercial aerospace, business jet, military and energy markets.

Image Source: Zacks Investment Research

Catalysts Behind the Price Surge

Let’s delve deeper to unearth the factors working in favor of this Zacks Rank #1 (Strong Buy) stock.

The company’s performance benefits from robust momentum in the Aerospace segment owing to higher commercial OEM and aftermarket sales resulting from improving passenger traffic and fleet utilization.

The Aerospace segment is likely to benefit from a rise in U.S. defense spending due to increasing geopolitical tensions and a minor increase in U.S. defense procurement. Also, the industrial segment is benefiting from solid demand for power generation and continued demand for backup power. Aerospace revenues are now suggested to rise between 16% and 18%, while Industrial revenues are forecasted to climb in the band of 28-30%. Earlier, both segments’ revenues were anticipated to improve between 14% and 19%.

The company plans to shift some of the machine components to its own factories/capable third-party suppliers to reduce cost and lead time and improve quality. Also, the company continues to invest in research and development to minimize fuel consumption and emissions, aid clients in tackling increasing fuel and motion control challenges, and help them develop clean fuel for running engines.

For fiscal 2023, the company expects net sales in the band of $2.85-$2.9 billion compared with the earlier guided range of $2.7-$2.8 billion. Earnings per share (EPS) is estimated to be in the range of $4.05-$4.25 compared with the previous view of $3.50-$3.75.

The Zacks Consensus Estimate for fiscal 2023 and 2024 earnings has increased 15.6% and 10.5%, respectively, in the past 60 days, reflecting analysts’ optimism regarding the company’s prospects.

Despite strong demand, continued softness in defense OEM sales due to lower guided weapons sales and supply-chain disruptions are major headwinds. Global macroeconomic weakness, forex volatility and rising costs are added concerns.

Other Stocks to Consider

Some other top-ranked stocks in the broader technology space are Asure Software ASUR, Aspen Technology AZPN and Badger Meter BMI. Asure Software presently sports a Zacks Rank #1, whereas Badger Meter and Aspen Technology currently carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Asure Software’s 2023 EPS has increased 35% in the past 60 days to 54 cents.

Asure Software’s earnings beat the Zacks Consensus Estimate in all the last four quarters, the average being 376.4%. Shares of ASUR have surged 66.7% in the past year.

The Zacks Consensus Estimate for Aspen Technology’s fiscal 2024 EPS has increased 5.8% in the past 60 days to $6.58.

Aspen Technology’s long-term earnings growth rate is 17.1%. Shares of AZPN have declined 12.6% in the past year.

The Zacks Consensus Estimate for Badger Meter’s 2023 EPS has increased 6.3% in the past 60 days to $2.86.

Badger Meter’s earnings beat the Zacks Consensus Estimate in all the last four quarters, the average being 6.7%. Shares of BMI have surged 69.5% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Badger Meter, Inc. (BMI) : Free Stock Analysis Report

Asure Software Inc (ASUR) : Free Stock Analysis Report

Woodward, Inc. (WWD) : Free Stock Analysis Report

Aspen Technology, Inc. (AZPN) : Free Stock Analysis Report