Is It Worth Considering Dun & Bradstreet Holdings, Inc. (NYSE:DNB) For Its Upcoming Dividend?

Dun & Bradstreet Holdings, Inc. (NYSE:DNB) is about to trade ex-dividend in the next 4 days. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. This means that investors who purchase Dun & Bradstreet Holdings' shares on or after the 6th of March will not receive the dividend, which will be paid on the 21st of March.

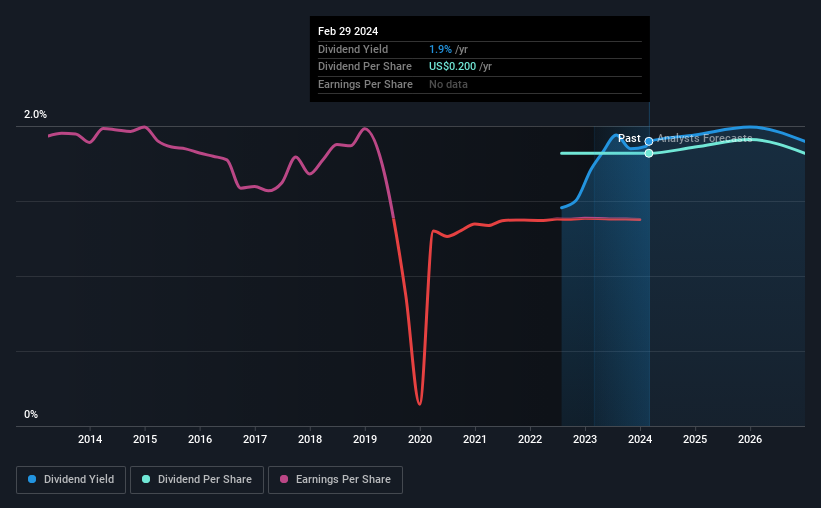

The company's next dividend payment will be US$0.05 per share, on the back of last year when the company paid a total of US$0.20 to shareholders. Looking at the last 12 months of distributions, Dun & Bradstreet Holdings has a trailing yield of approximately 1.9% on its current stock price of US$10.54. If you buy this business for its dividend, you should have an idea of whether Dun & Bradstreet Holdings's dividend is reliable and sustainable. So we need to investigate whether Dun & Bradstreet Holdings can afford its dividend, and if the dividend could grow.

See our latest analysis for Dun & Bradstreet Holdings

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Dun & Bradstreet Holdings's dividend is not well covered by earnings, as the company lost money last year. This is not a sustainable state of affairs, so it would be worth investigating if earnings are expected to recover. Considering the lack of profitability, we also need to check if the company generated enough cash flow to cover the dividend payment. If cash earnings don't cover the dividend, the company would have to pay dividends out of cash in the bank, or by borrowing money, neither of which is long-term sustainable. It distributed 34% of its free cash flow as dividends, a comfortable payout level for most companies.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Dun & Bradstreet Holdings was unprofitable last year, but at least the general trend suggests its earnings have been improving over the past five years. Even so, an unprofitable company whose business does not quickly recover is usually not a good candidate for dividend investors.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. It looks like the Dun & Bradstreet Holdings dividends are largely the same as they were two years ago.

We update our analysis on Dun & Bradstreet Holdings every 24 hours, so you can always get the latest insights on its financial health, here.

The Bottom Line

Is Dun & Bradstreet Holdings an attractive dividend stock, or better left on the shelf? First, it's not great to see the company paying a dividend despite being loss-making over the last year. On the plus side, the dividend was covered by free cash flow." In summary, while it has some positive characteristics, we're not inclined to race out and buy Dun & Bradstreet Holdings today.

With that in mind, a critical part of thorough stock research is being aware of any risks that stock currently faces. We've identified 2 warning signs with Dun & Bradstreet Holdings (at least 1 which can't be ignored), and understanding them should be part of your investment process.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.