Zevia PBC's (NYSE:ZVIA) Q4 Sales Top Estimates But

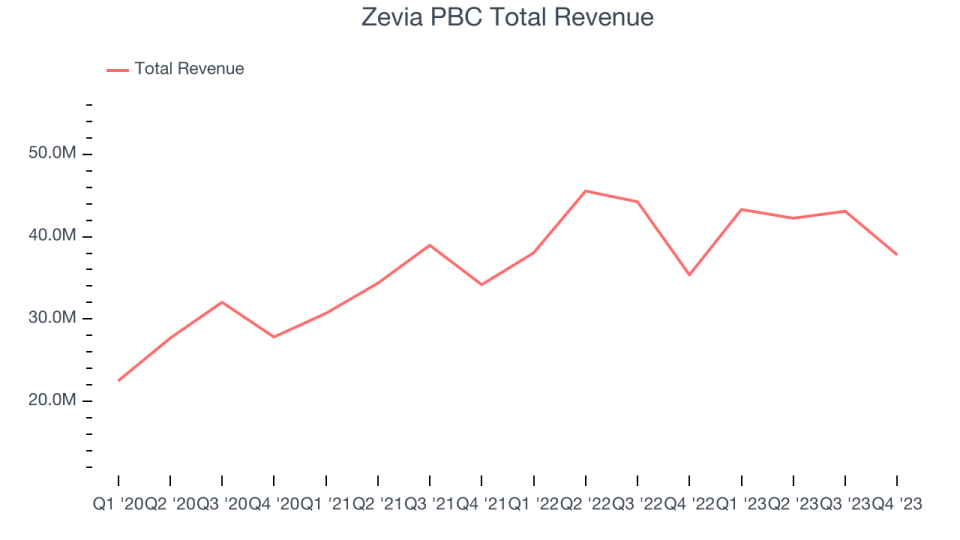

Beverage company Zevia (NYSE:ZVIA) reported Q4 FY2023 results topping analysts' expectations , with revenue up 6.9% year on year to $37.79 million. On the other hand, next quarter's revenue guidance of $39 million was less impressive, coming in 19.8% below analysts' estimates. It made a GAAP loss of $0.14 per share, down from its loss of $0.08 per share in the same quarter last year.

Is now the time to buy Zevia PBC? Find out by accessing our full research report, it's free.

Zevia PBC (ZVIA) Q4 FY2023 Highlights:

Revenue: $37.79 million vs analyst estimates of $37.35 million (1.2% beat)

EPS: -$0.14 vs analyst estimates of -$0.14 (2% beat)

Revenue Guidance for Q1 2024 is $39 million at the midpoint, below analyst estimates of $48.62 million

Free Cash Flow was -$6.67 million compared to -$10.76 million in the previous quarter

Gross Margin (GAAP): 40.7%, down from 44.3% in the same quarter last year

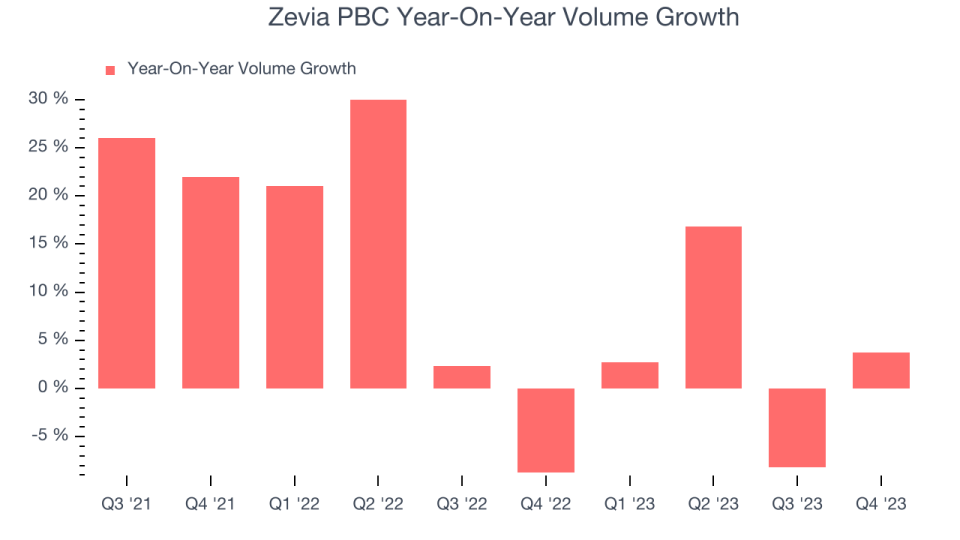

Sales Volumes were up 3.7% year on year (beat vs. expectations of flattish growth)

Market Capitalization: $81.16 million

“Our fourth quarter volume growth reflects continued underlying consumer demand, a healthy business within our core customer base and exciting growth levels with developing customers,” said Amy Taylor, President and Chief Executive Officer.

With a primary focus on soda but also a presence in energy drinks and teas, Zevia (NYSE:ZVIA) is a better-for-you beverage company.

Beverages and Alcohol

The beverages and alcohol category encompasses companies engaged in the production, distribution, and sale of refreshments like beer, wine, and spirits, along with soft drinks, juices, and bottled water. These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the explosion of alcoholic craft beer drinks or the steady decline of non-alcoholic sugary sodas. The industry is highly competitive, with a diverse range of products from large multinational corporations, niche brands, and startups vying for market share. It's also subject to varying degrees of government regulation and taxation, especially for alcoholic beverages.

Sales Growth

Zevia PBC is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale.

As you can see below, the company's annualized revenue growth rate of 14.8% over the last three years was solid for a consumer staples business.

This quarter, Zevia PBC reported solid year-on-year revenue growth of 6.9%, and its $37.79 million in revenue outperformed Wall Street's estimates by 1.2%. The company is guiding for a 9.9% year-on-year revenue decline next quarter to $39 million, a reversal from the 13.8% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 14.3% over the next 12 months, an acceleration from this quarter.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Zevia PBC's average quarterly volume growth was a robust 7.5% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

In Zevia PBC's Q4 2023, sales volumes jumped 3.7% year on year. This result was a well-appreciated turnaround from the 8.7% year-on-year decline it posted 12 months ago, showing the company is heading in the right direction.

Key Takeaways from Zevia PBC's Q4 Results

It was encouraging to see Zevia PBC narrowly top analysts' revenue expectations this quarter on better volumes. On the other hand, its revenue guidance for next quarter missed analysts' expectations. Overall, this was a mixed quarter for Zevia PBC. The company is down 1.9% on the results and currently trades at $1.58 per share.

Zevia PBC may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.