Zions' (ZION) Loans & Higher Rates Aid Amid Poor Asset Quality

A decent loan balance, a rise in revenues and higher interest rates are expected to support Zions Bancorporation’s ZION financials. However, elevated expenses and worsening asset quality amid an uncertain macroeconomic outlook are major headwinds.

ZION has been witnessing persistent organic growth. The company’s total revenues witnessed a compound annual growth rate (CAGR) of 3.4% over the last three years ended 2022 despite witnessing a fall in total revenues in 2020. The upward trend continued in the first nine months of 2023.

However, as the operating environment is expected to remain challenging in the near term, revenue growth is likely to be subdued. We project total revenues to decline 1.1% and 4.8% in 2023 and 2024, respectively, before rebounding and growing 3.3% in 2025.

Net loans and leases (net of unearned income and fees) witnessed a CAGR of 4.5% for the last three years (2019-2022). The uptrend continued for the same in the first nine months of 2023. Our estimates for total loans suggest a CAGR of 1.4% by 2025.

Given the high interest rate environment, ZION’s net interest margin (NIM) is likely to witness a decent expansion despite a rise in deposit costs. We project NIM to be 2.96% for 2023.

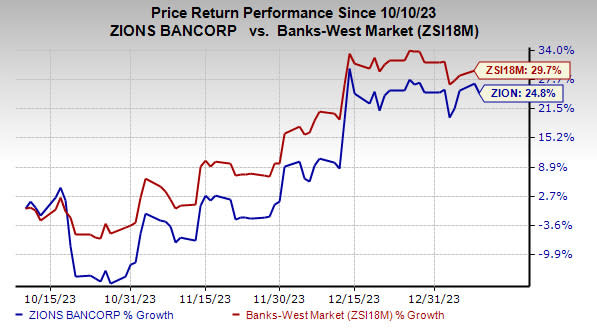

Over the past three months, shares of this Zacks Rank #3 (Hold) company have rallied 24.8% compared with the industry’s growth of 29.7%.

Image Source: Zacks Investment Research

However, Zions has been witnessing a persistent rise in expenses. Though total non-interest expenses declined in 2020, it recorded a positive CAGR of 2.5% over the last three years (ended 2022). The same trend persisted in the first nine months of 2023. Higher salaries and employee benefit costs were the primary reasons behind elevated expenses.

As the company continues to invest in franchises and digitize operations, expenses are expected to remain elevated in the quarters ahead. Our estimates for non-interest expenses suggest a CAGR of 3.3% by 2025.

ZION’s asset quality has been weakening over the past few years. Provision for credit losses increased in 2022 and in the first nine months of 2023 as the company continued to build reserves to combat the tough operating environment. We project provisions for credit losses to surge 58.5% in 2023.

Bank Stocks Worth Considering

A couple of better-ranked stocks from the banking space are Associated Bancorp ASB and OP Bancorp OPBK, each currently carrying a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Earnings estimates for ASB have been revised 1.3% upward for 2023 over the past 60 days. The company’s shares have gained 30.6% over the past three months.

The consensus estimate for OPBK’s 2023 earnings has been revised marginally upward over the past 30 days. Over the past three months, the company’s share price has increased 23.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zions Bancorporation, N.A. (ZION) : Free Stock Analysis Report

Associated Banc-Corp (ASB) : Free Stock Analysis Report

OP Bancorp (OPBK) : Free Stock Analysis Report