What Is ZoomerMedia's (CVE:ZUM) P/E Ratio After Its Share Price Rocketed?

ZoomerMedia (CVE:ZUM) shareholders are no doubt pleased to see that the share price has had a great month, posting a 50% gain, recovering from prior weakness. However, that doesn't change the fact that longer term shareholders might have been mercilessly wrecked by the 52% share price decline throughout the year.

Assuming no other changes, a sharply higher share price makes a stock less attractive to potential buyers. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. So some would prefer to hold off buying when there is a lot of optimism towards a stock. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

See our latest analysis for ZoomerMedia

How Does ZoomerMedia's P/E Ratio Compare To Its Peers?

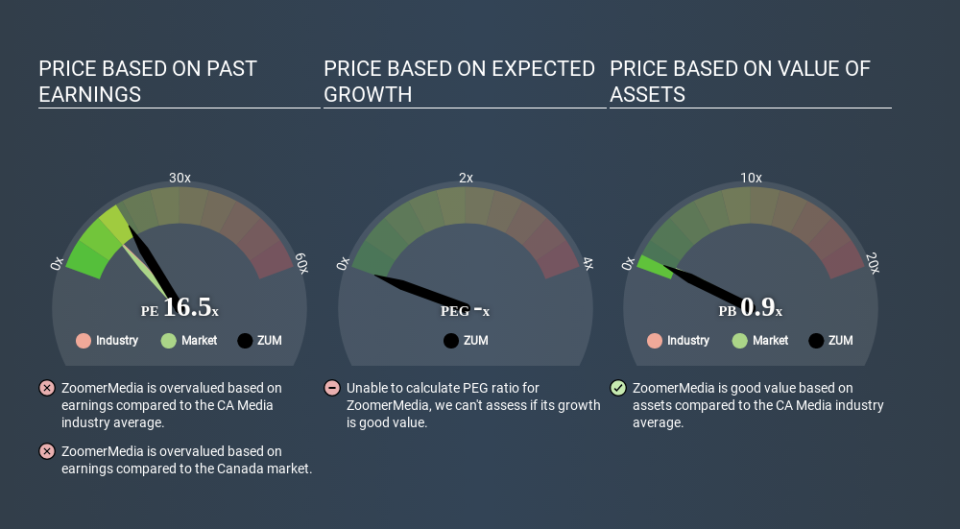

We can tell from its P/E ratio of 16.49 that there is some investor optimism about ZoomerMedia. As you can see below, ZoomerMedia has a higher P/E than the average company (12.2) in the media industry.

Its relatively high P/E ratio indicates that ZoomerMedia shareholders think it will perform better than other companies in its industry classification. The market is optimistic about the future, but that doesn't guarantee future growth. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

Companies that shrink earnings per share quickly will rapidly decrease the 'E' in the equation. Therefore, even if you pay a low multiple of earnings now, that multiple will become higher in the future. A higher P/E should indicate the stock is expensive relative to others -- and that may encourage shareholders to sell.

In the last year, ZoomerMedia grew EPS like Taylor Swift grew her fan base back in 2010; the 296% gain was both fast and well deserved. The sweetener is that the annual five year growth rate of 77% is also impressive. So I'd be surprised if the P/E ratio was not above average. Regrettably, the longer term performance is poor, with EPS down -77% per year over 3 years.

Remember: P/E Ratios Don't Consider The Balance Sheet

Don't forget that the P/E ratio considers market capitalization. In other words, it does not consider any debt or cash that the company may have on the balance sheet. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

How Does ZoomerMedia's Debt Impact Its P/E Ratio?

ZoomerMedia has net cash of CA$15m. This is fairly high at 38% of its market capitalization. That might mean balance sheet strength is important to the business, but should also help push the P/E a bit higher than it would otherwise be.

The Verdict On ZoomerMedia's P/E Ratio

ZoomerMedia's P/E is 16.5 which is above average (11.9) in its market. Its net cash position is the cherry on top of its superb EPS growth. So based on this analysis we'd expect ZoomerMedia to have a high P/E ratio. What is very clear is that the market has become significantly more optimistic about ZoomerMedia over the last month, with the P/E ratio rising from 11.0 back then to 16.5 today. If you like to buy stocks that have recently impressed the market, then this one might be a candidate; but if you prefer to invest when there is 'blood in the streets', then you may feel the opportunity has passed.

Investors have an opportunity when market expectations about a stock are wrong. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Of course you might be able to find a better stock than ZoomerMedia. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.