Many people cannot remember the last time they stepped into a bank branch.

Yet the largest U.S. banks are racing each other to build hundreds of branches in new cities across the country, showing that the brick-and-mortar model isn’t dead — it’s just evolving.

On their third-quarter earnings calls, the two largest U.S. retail banks – JPMorgan Chase (JPM) and Bank of America (BAC) — pledged expansions into new cities with a flurry of new physical branches. The CEOs of both companies say that while mobile banking is still important, they see plenty of markets where they can grab market share through new stores.

Opportunity

Both banks are making moves as the next two largest banks — Wells Fargo (WFC) and Citigroup (C) — pump the brakes on their branch growth.

Wells Fargo, hobbled by an asset cap from the Federal Reserve amid its reputational issues, has said it will shrink its branch network by about 800 locations by 2020. Company CFO John Shrewsberry said on a third-quarter call that they are on track to close about 300 branches this year. While most will be consolidated, 52 of the planned branches will be sold.

Citi, meanwhile, is focused on pausing its branch expansion while it measures its online performance. The company said that it will build new branches if it sees heavy credit card client use in concentrated cities, but said digital activity will determine their focus.

“Whether we do it out of a Branch on Fifth Avenue or whether we do it online, we’ve got the same connectivity to the products,” Citi CEO Michael Corbat said.

Enter: JPMorgan Chase and Bank of America.

Applications filed with the Office of the Comptroller of the Currency show that Chase Bank has proposed 161 new locations in the last year, a number of which are in new cities like Boston, Philadelphia and Washington, D.C. Yahoo Finance reported that the company is also planning new stores in Minneapolis, Nashville, Kansas City and Raleigh.

“Every time we open branches in a new market we bring the full force of JPMorgan Chase to that community,” JPMorgan Chase CEO Jamie Dimon said in the company’s third-quarter earnings release.

Bank of America, which has about 500 fewer retail stores than Chase, is prioritizing a build-out of its existing presence in the few large cities where it not among the top three banks in terms of deposit market share: Denver, Minneapolis, Indianapolis and Pittsburgh.

“A digital-only institution, in our mind, is not the way that you should go,” Bank of America CEO Brian Moynihan said.

Minnesota nice

One battleground in the branch fight is in Minneapolis, where JPMorgan Chase and Bank of America are both mounting an attack on U.S. Bancorp (USB), the fifth largest U.S. commercial bank.

But the Twin Cities-based U.S. Bancorp is doubling down on digital banking. At a conference in September, U.S. Bancorp CEO Andy Cecere said the company would be shrinking its physical footprint and using its mobile app to reach markets where it has few or no branches. Cecere listed Texas, Florida and North Carolina as examples of new frontiers for U.S. Bancorp — areas where both Chase and Bank of America compete.

But Cecere said that the branch is still important, and said the company would continue to prioritize its presence in smaller towns where the only other competition is community banks.

“That combination of digital capabilities together with the physical presence is the way we think about the future,” Cecere said.

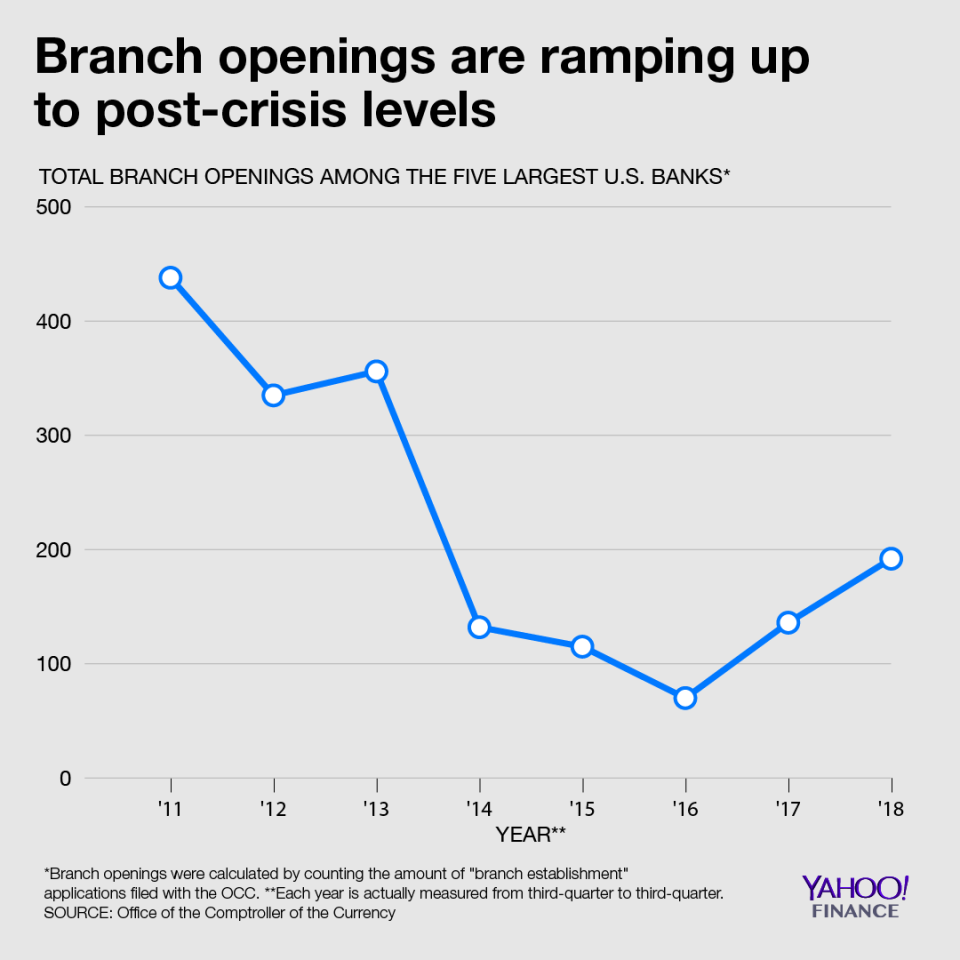

On the whole, the five largest banks are still consolidating and closing more branches than they are opening, but the pace of openings appears to be picking up.

Rob Berini, a managing director with Deloitte Consulting’s banking group, says the branch model is far from dead, but acknowledged that every company is attempting a different balance of physical and digital banking.

“It’s an experiment and banks are having different results,” Berini said.

Read more:

Fed Vice Chair Quarles prefers ‘more gradual’ rate hikes

Prudential Financial to shed its post-crisis ‘too big to fail’ label