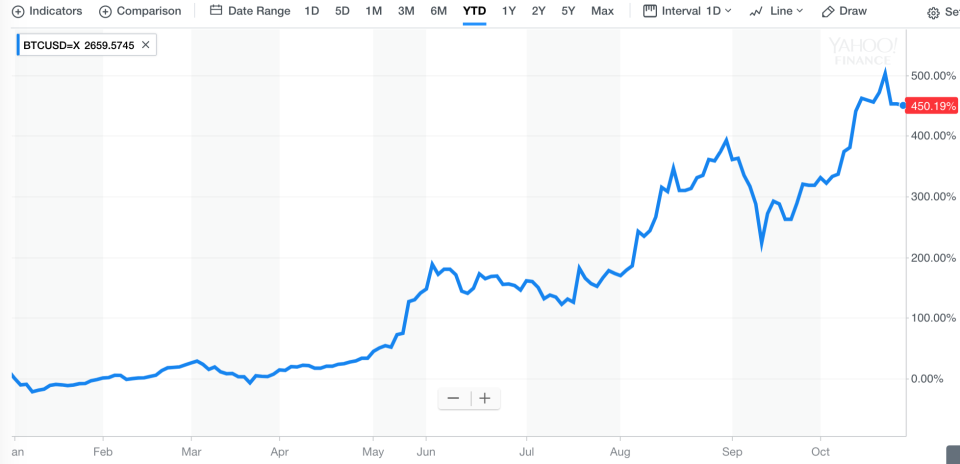

The digital currency bitcoin keeps hitting new record highs. It topped $6,100 per coin earlier this week. That gave it a $100 billion market cap. It’s up 450% in 2017 so far, and 50% in the past month. Clearly, speculative investors believe in bitcoin right now.

Big names in finance keep dismissing it anyway.

JPMorgan Chase CEO Jamie Dimon called bitcoin a “fraud” and said it’s “worse than tulip bulbs.” Ray Dalio, founder of hedge fund Bridgewater Associates, called it a “bubble” because, “You can’t spend it very easily” and “the amount of speculation that is going on and the lack of transactions.” Saudi billionaire Prince Alwaleed bin Talal said bitcoin, “doesn’t make sense… I think this is Enron in the making.”

While it is in fashion to brush off bitcoin, some of the very same names have voiced enthusiasm around blockchain, the distributed ledger technology that underlies bitcoin and originated with bitcoin in 2009.

Dimon himself has publicly said he sees potential in blockchain tech, and his company just announced this month the launch of a blockchain-based pilot to “significantly reduce” the number of entities needed to verify global payments, which would cut down transaction settlement times.

While Jamie Dimon of @jpmorgan was bashing #bitcoin, his SF office was hosting @blockchaincap @PanteraCapital @BoostVC and @polychainfund pic.twitter.com/0D6Ul1YSdy

— Bart Stephens (@pbartstephens) September 12, 2017

In fact, blockchain fever has taken hold all over Wall Street. To name only a few: JPMorgan Chase, Goldman Sachs, Bank of America, Citi, and Visa are all doing some form of pilot testing with blockchain. Startups like Chain, itBit, and Digital Asset, which build private blockchain solutions for enterprise, are some of the hottest and best-funded fintech companies around.

Even Walmart is now using blockchain to track food shipments.

The fallacy of “blockchain without bitcoin”

There’s a paradox inherent in raving about blockchain but disparaging bitcoin, since the two originated together.

As many in the bitcoin world will tell you, the type of closed, permissioned systems that banks are testing defeat the point of the bitcoin blockchain, which is open and permissionless. They say there must be some form of digital token associated with a ledger in order for the system to work, as a way to dole out incentive to the machines recording transactions. (On the bitcoin blockchain, miners are rewarded with a small amount of bitcoin every time they upload a bundle of transaction records, called “blocks,” to the blockchain.)

For now, the way that banks are using blockchains, as a way to speed up and improve their back-end record-keeping, is not particularly revolutionary, but merely an incremental improvement in efficiency. (And yet the word itself, “blockchain,” manages to impress investors.)

“At the end of the day, it’s not a very exciting innovation,” Jerry Brito, executive director of the cryptocurrency non-profit Coin Center, told Yahoo Finance. “The real innovation is a completely open and global ledger that is permission-less. Having a closed, permissioned ledger run by banks, that might allow for better auditing but there’s no innovation there.”

"Major banks complete first international transaction using a blockchain"

You mean, the same thing bitcoin has done several million times?

— Andreas M. Antonopoulos (@aantonop) October 24, 2016

Regardless of the blockchain hype (which is unlikely to die down any time soon), to dismiss bitcoin as a fraud shows a lack of understanding: bitcoin is a technology. It is neutral; there are criminal use cases and socially conscious use cases alike.

Similarly, those who dismiss bitcoin because it can’t be spent as payment in many mainstream places are also missing the point. It may be the case that “currency” isn’t the best word for bitcoin, but rather “digital asset” or “token.”

While people like to talk about needing a “killer application” for bitcoin that would show its value to the mainstream economy, it is likely that bitcoin itself is the killer app. After all, the coin has created nearly $100 billion in value from nothing.

Its steady rise in value alone — up more than 3,000% over the past five years — is an indication that the interest isn’t waning, so financial markets can’t look away. And as payment leaders like MasterCard push for the death of cash, bitcoin is getting us closer to that time. For many people, their money is already entirely digital anyway, numbers on a screen. (In the first episode of the show “Mr. Robot,” Christian Slater’s character makes a similar point: “Money hasn’t been real since we got off the gold standard. It’s become virtual. Software.”)

A safe haven during economic turmoil

Bitcoin’s most obvious use case, the significance of which is instantly clear, is for sending money across borders with minimal fees and minimal transfer delays. Bitcoin has repeatedly saved people’s finances in emergency situations. During the Greek bank crisis in 2015, or in Venezuela this year, regular people have sought safe haven in bitcoin when their national currency was failing. It is why China’s central bank has cracked down on bitcoin as a way to restrict capital outflows and buoy the yuan.

Bitcoin’s anonymity can also be a benefit in certain situations, such as charitable donations to organizations the government does not support (think WikiLeaks) or anonymous investment support. Morgan Stanley CEO James Gorman has pinpointed this aspect specifically: “The concept of anonymous currency is a very interesting concept,” he said, “interesting for the privacy protections it gives people, interesting because what it says to the central banking system about controlling that.”

Then there are companies using bitcoin as the vehicle for something much bigger than cross-border payments or anonymous online purchases. Balaji Srinivasan at 21 Inc wants to create a “machine economy” where machines can ping each other with payment requests, in bitcoin, every time a machine visits a certain URL. You can imagine the possibilities for micro-payments, reducing the friction of entering your payment info on every website, and paying for online content like news.

Not everyone in the finance world is sour on bitcoin. Fidelity will link customer accounts to their Coinbase bitcoin wallets, and Fidelity CEO Abby Johnson says, “I’m a believer. I’m one of the few standing before you today from a large financial services company that has not given up on digital currencies.” Goldman Sachs is considering launching a bitcoin trading business. Even Larry Fink has said that if money were to go truly digital, “we would not have money laundering anymore.”

Ethereum and the rise of altcoins

Much like how Uber may not necessarily be the eventual big winner in the taxi app space just because it was first, bitcoin may not be the top cryptocurrency in a few years (though it likely will). But even if bitcoin were to lose favor — if it were to crash and stay down, say, or if the bitcoin blockchain experienced a terrible failure — its permanent, lasting influence is now clear.

Bitcoin has engendered a plethora of additional cryptocurrencies or “altcoins,” many of which are now significant in their own right. (And for that reason, some proponents resent the word “altcoin” since it implies they’re all automatically “lesser than” bitcoin.) Litecoin has a market cap near $3 billion, Dashcoin is at $2.2 billion, and Zcash approaches $1 billion. Ripple, the settlement token of the Ripple network, has a market cap of nearly $8 billion.

1/ If you consider all #cryptoassets outside of #bitcoin to be “altcoins” or “alts,” then you are missing the bigger picture.

— Chris Burniske (@cburniske) October 22, 2017

But above all of those, second only to bitcoin, is ether, the coin of the Ethereum blockchain. Its market cap is nearly $28 billion, a stunning figure considering that Ethereum only launched (by mining its “genesis block” or first transaction bundle) in 2015. The significance of Ethereum is not in its token, but in the ability to store smart contracts on its ledger—the Ethereum blockchain was designed specifically for that purpose.

The faith in the potential of the Ethereum chain is so high that the typical ICO (initial coin offering), a model for crypto startups to raise money via token sale, is built on the back of Ethereum. The model is: you buy a new startup’s own token, for later use within its ecosystem, and pay in ether (or, in many cases, bitcoin, if you choose). While investing in an ICO carries high risk, the model has already raised more than $1 billion in funding this year so far.

That is just one more influence bitcoin has had, among many. And the coin isn’t going anywhere just yet, no matter how many finance titans rail that it is a bubble or scam.

Disclosure: The author owns less than 1 bitcoin, purchased in 2015 for reporting purposes.

—

Daniel Roberts covers bitcoin and blockchain at Yahoo Finance. Follow him on Twitter at @readDanwrite.

Read more:

Japan is poised to become the leading bitcoin market

Why China’s central bank fears bitcoin

Why Ethereum is the hottest new thing in digital currency

More than 75 banks are now on Ripple’s blockchain network

Expect more blockchain hype in 2017

Here’s why 21 Inc. is the most exciting bitcoin company right now

How bitcoin company Coinbase is staying relevant amid the blockchain craze