Constellation Brands Shares a Value Amid Weak Momentum, Upcoming Earnings

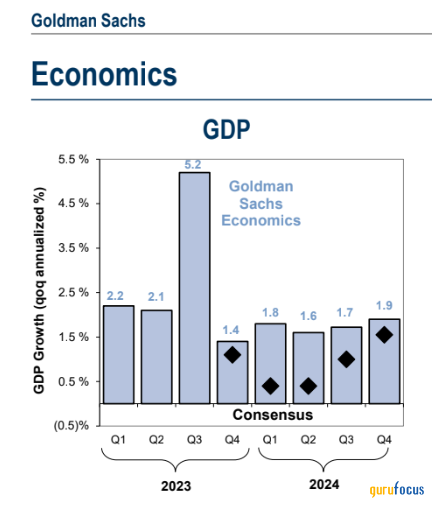

There are concerns about the strength of the consumer as 2024 gets going. Credit card use is up while debt delinquencies are on the rise, though they are generally not far from what we saw pre-pandemic. As U.S. real gross domestic product growth possibly eases over the first half of this year, keeping close tabs on reports such as retail sales and monthly jobs numbers is key. Additionally, we will get a fresh slate of corporate earnings reports to parse through later this month. One company in the consumer staples sector reports quarterly results before the big banks kick off traditional earnings season.

I see shares of Constellation Brands Inc. (NYSE:STZ) as undervalued, but am concerned that technicals could lead shares lower over the coming weeks.

U.S. real GDP growth seen troughing in Q1-Q2 near +0.4%

Company description

According to Bank of America Global Research, Constellation Brands is one of the world's leading producers of alcoholic beverage brands. It markets wines, spirits and imported beer globally and is known for its premium wine labels. Among its most well-known brands include Robert Mondavi, Clos du Bois, Blackstone, Arbor Mist and Svedka vodka. It also sells Corona brand beers and Modelo Especial with a heavy presence in the Mexico market.

Key data

Yielding a $44.4 billion market cap, the New York-based distiller and vintner company within the consumer staples sector trades at a near-market 20.3 forward non-GAAP price-earnings ratio and pays a modest 1.5% forward dividend yield as of Dec. 29. Ahead of earnings due out on Friday, Jan. 5, shares trade with a moderate 24% implied volatility percentage, while short interest on the stock is modest at just 0.9%.

Data from Option Research & Technology Services shows the expected earnings-related stock price swing is 3.3% when assessing the nearest-expiring at-the-money straddle following the third-quarter 2024 report. Analysts expect $3 of operating earnings per share, which would be a 6% increase from $2.83 reported in the period a year ago.

Color on the quarter

Back in October, Constellation reported a solid second-quarter report. Non-GAAP earnings per share verified at $3.70, topping the Wall Street consensus expectation of $3.37, while revenue of $2.8 billion jumped close to 7% compared to year-ago levels, a small beat. The management team lifted its 2024 GAAP earnings outlook to $9.60 to $9.80 with non-GAAP earnings seen coming in between $12 and $12.20.

The company reaffirmed its cash flow outlook while declaring a quarterly dividend of 89 cents. Excluding losses from its stake in Canopy Growth (NASDAQ:CGC), the quarter was generally strong as sales trends of both its beer and wine and spirit segments were encouraging. Beer shipment growth was up 8.7% year over year, though the wine and spirits segment's operating income was less impressive.

Then in November, the company approved a $2 billion stock buyback plan, but that did not do much to help the stock price. Still, Constellation remains one of 37 high-growth names that are overweight recommended by analysts at Morgan Stanley, while Goldman Sachs identified it as one of just six stocks poised to outperform in 2024 due to brand resonance, strong scalability and a robust business model.

Key risks and peer analysis

Key risks for Constellation include new brands eating into profits of its existing products, further weakness with Canopy Growth and an overall risk-on investing environment that could favor more discretionary industries. Compared to its peers, the company features a middle-of-the-road valuation while growth trends should be better going forward. Constellation features industry-leading profitability with consistent free cash flow. Still, share price momentum has been relatively weak versus its competitors.

Valuation

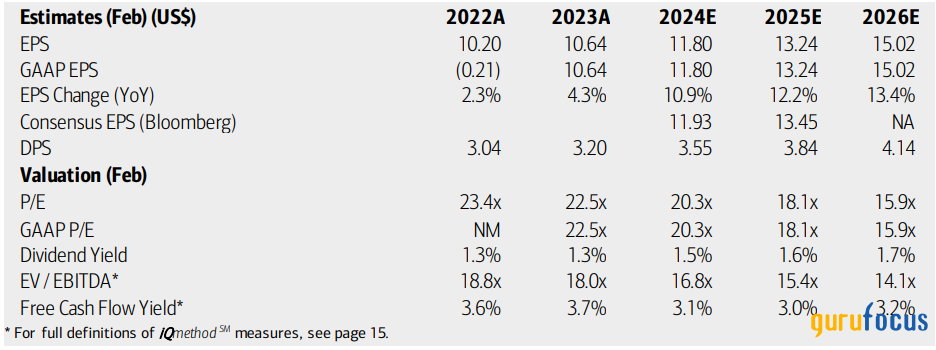

On valuation, analysts at Bank of America see earnings growth accelerating to nearly 11% in the current fiscal year while per-share profits are then expected to continue rising, perhaps towards a 13% annual rate by the out years. The current consensus outlook calls for more than $15 of earnings per share by 2026 as the top-line advances at a steady 6% to 7% rate over the next two years.

Dividends, meanwhile, are forecasted to climb at a healthy pace over the coming quarters while free cash flow per share hovers somewhat low at 3%. With current earnings multiples around 20, the stock appears to be fully priced and its enterprise value/Ebitda ratio is at a slight premium compared to that of the S&P 500.

If we apply Constellation's five-year average non-GAAP price-earnings ratio of 21.5 and assume normalized earnings of $12.80 per share, then shares should be priced near $275, making it a decent bargain today considering its robust earnings growth trajectory and defensive nature. Its forward non-GAAP PEG ratio is also 18% below its long-term average.

Constellation Brands: Earnings, valuation, free cash flow and dividend yield forecasts

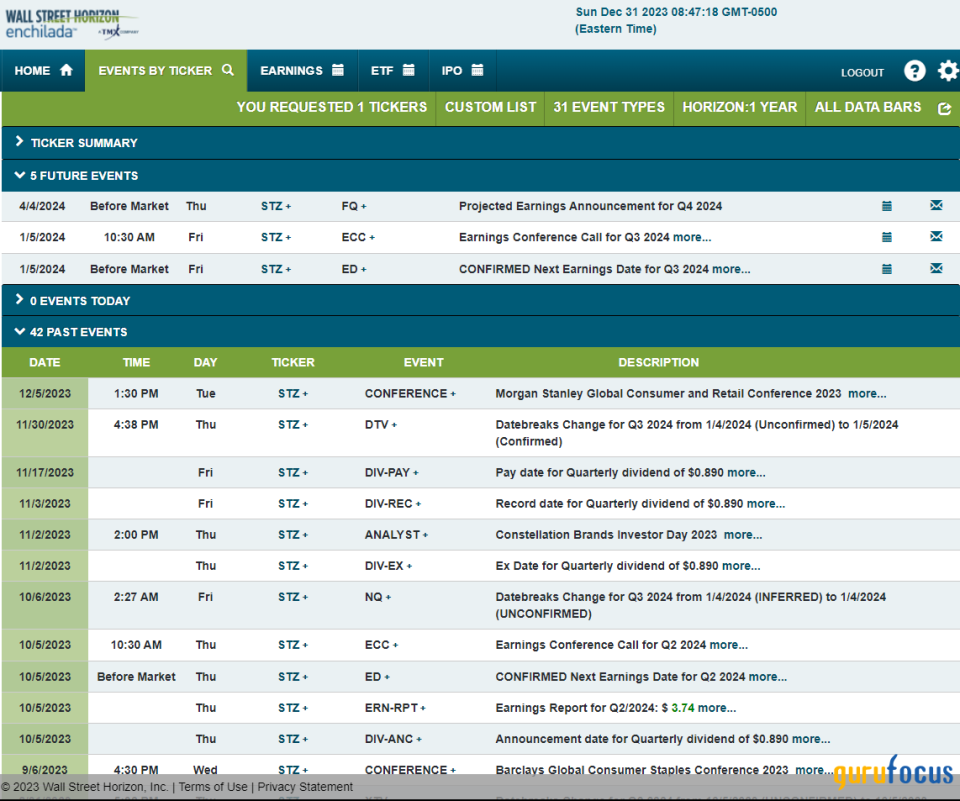

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed third-quarter 2024 earnings date of Friday, Jan. 5. The company hosts an earnings conference call later that morning you can listen live here. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

The technical take

Constellation Brands has severely underperformed the broad market since late July. Notice in the long-term chart below that shares peaked above $270 to notch an all-time high last summer, but then failed to build on that momentum over the back half of 2023. It even managed to lose out to the underperforming Consumer Staples sector ETF (XLP) over the past five months. Technicians generally like to see follow-through when a new high is made, so the last handful of months have not been encouraging from a momentum point of view. Moreover, the series of higher highs without a definitive breakout is not the healthiest setup for a strong uptrend, though there is apparent support along the rising 200-week moving average as well as the $207 to $210 area.

In the near term, I spot a bear flag pattern that began in October. Following the dramatic selloff from late July through the end of the third quarter, the stock has consolidated and the implication is that the broader trend will continue lower in this case. Also take a look at the volume by price indicator on the left side of the graph there is an ample amount of shares traded in the $210 to $240 zone, so pullbacks toward the low $200s should be seen as a buying opportunity, in my view.

Overall, Constellation's momentum situation is not ideal from the bulls' perspective and a buy the dip strategy could be more prudent right now rather than buying at current levels.

Solid support in the low $200s, near-term bear flag

The bottom line

I see fundamental upside to Constellation Brands given its current and historical valuation. Its defensive nature and premium brands should hold up well if we see a shaky macro backdrop in 2024. Concerning me are some negative technical features, though support on the chart is apparent about 10% to 15% lower than 2023's closing price.

This article first appeared on GuruFocus.