Sprouts Farmers (SFM) Q3 Earnings Beat, Comps Up 3.9% Y/Y

Sprouts Farmers Market, Inc. SFM came up with third-quarter 2023 results, wherein the top and bottom lines not only increased year over year but also beat their respective Zacks Consensus Estimate. Following the results, management raised the full-year view.

Q3 in Details

The renowned grocery retailer delivered adjusted quarterly earnings of 65 cents a share, which cruised past the Zacks Consensus Estimate of 62 cents. Impressively, the bottom line increased 6.6% from the 61 cents reported in the year-ago period.

Net sales of this Phoenix, AZ-based company came in at $1,713.3 million, which came ahead of the Zacks Consensus Estimate of $1,681 million. The metric increased 7.6% on a year-over-year basis. The growth was driven by sales from the new stores and a jump in comparable store sales.

Comparable store sales increased 3.9% during the quarter under review, better than our estimate of a 2% jump. We note that e-commerce sales grew 16% and represented 12.1% of total sales in the quarter.

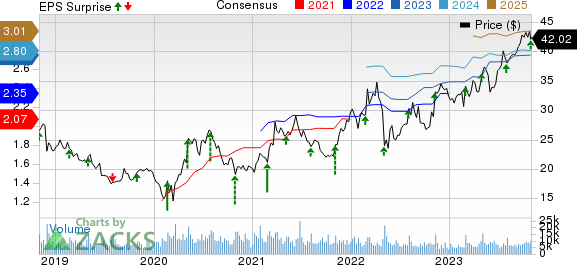

Sprouts Farmers Market, Inc. Price, Consensus and EPS Surprise

Sprouts Farmers Market, Inc. price-consensus-eps-surprise-chart | Sprouts Farmers Market, Inc. Quote

Margins

The adjusted gross profit rose 7.4% year over year to $626.7 million in the quarter. The adjusted gross margin contracted about 10 basis points to 36.6% from the prior-year quarter. We had expected the gross margin to remain unchanged compared with the year-ago period.

Sprouts Farmers reported an adjusted operating income of $90 million, marginally down from the $90.4 million reported in the year-ago period. The adjusted operating margin decreased 40 basis points to 5.3%. We had anticipated a 50-basis point contraction in the operating margin.

SG&A expenses increased 9.1% year over year to $502.8 million. Excluding the impact of special items, adjusted SG&A expenses totaled $502 million, an increase of $41 million from the year-ago period and representing roughly 30 basis points of deleverage due to new store openings, wage increases and labor investments in the Store Sampling program.

Store Update

During the quarter, Sprouts Farmers opened 10 new stores, thereby taking the total count to 401 stores in 23 states as of Oct 1, 2023. The company plans to open 30 new stores in 2023.

Other Financial Aspects

Sprouts Farmers ended the year with cash and cash equivalents of $251.8 million, long-term debt and finance lease liabilities of roughly $158.9 million and stockholders’ equity of $1,115 million. The company repurchased 831 thousand shares for a total investment of $32 million in the quarter.

Sprouts Farmers generated cash from operations of $409 million and spent $157 million on capital expenditures, net of landlord reimbursement, year to date through Oct 1, 2023. Management anticipates capital expenditures (net of landlord reimbursements) in the range of $190-$210 million for 2023.

Outlook

Sprouts Farmers expects net sales growth of 6.5-7% and comparable store sales growth of 3% in 2023. The company earlier projected a net sales increase of 5-6% and comparable store sales growth of 2-3%.

Sprouts Farmers guided adjusted earnings before interest and taxes between $387 million and $393 million for 2023, up from its prior projection of $378 million to $390 million. It now foresees full-year adjusted earnings in the band of $2.77-$2.81 per share, up from the $2.39 reported in 2022, assuming no additional share repurchases. The company had earlier guided earnings between $2.68 and $2.76 per share.

For the fourth quarter, Sprouts Farmers expects comparable store sales growth of approximately 3% and adjusted earnings in the band of 42-46 cents a share compared with 42 cents reported in the year-ago period.

This Zacks Rank #3 (Hold) stock has risen 11% in the past six months against the industry’s decline of 0.5%.

3 Stocks Looking Red Hot

Here, we have highlighted three better-ranked stocks, namely Grocery Outlet GO, Ross Stores ROST and Walmart WMT.

Grocery Outlet, an extreme value retailer of quality, name-brand consumables and fresh products, currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Grocery Outlet’s current financial-year sales and earnings suggests growth of 11.2% and 4.9%, respectively, from the year-ago reported numbers. GO has a trailing four-quarter earnings surprise of 14.3%, on average.

Ross Stores, which operates off-price retail apparel and home fashion stores, currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Ross Stores’ current financial-year sales and earnings indicates growth of 7.1% and 19.4%, respectively, from the year-ago reported numbers. ROST has a trailing four-quarter earnings surprise of 11.4%, on average.

Walmart, which operates a chain of hypermarkets, discount department stores and grocery stores, currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Walmart’s current financial-year sales and earnings implies growth of 5% and 2.4%, respectively, from the year-ago reported numbers. WMT has a trailing four-quarter earnings surprise of 11.6%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT) : Free Stock Analysis Report

Ross Stores, Inc. (ROST) : Free Stock Analysis Report

Sprouts Farmers Market, Inc. (SFM) : Free Stock Analysis Report

Grocery Outlet Holding Corp. (GO) : Free Stock Analysis Report