NasdaqGS - Nasdaq Real Time Price • USD

Netflix, Inc. (NFLX)

At close: April 26 at 4:00 PM EDT

After hours: April 26 at 7:57 PM EDT

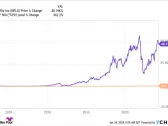

Performance Overview

Trailing total returns as of 4/26/2024, which may include dividends or other distributions. Benchmark is S&P 500

| Return | NFLX | S&P 500 |

|---|---|---|

| YTD | +15.27% | +6.92% |

| 1-Year | +74.00% | +25.26% |

| 3-Year | +11.01% | +22.00% |